Share this

by aaronroseman

The recent drops in US consumption expenditures make trucking companies fear this could exaggerate the soft freight market by further compressing freight demand and prices. The goal of this article is to put freight’s dependence on procyclical consumption into a broader historical perspective using both internal and external data. Our key takeaways are:

(i) in the previous US recession, overall freight tonnage declined as personal consumption declined. In the current recession environment, we are seeing falls in consumption but we have yet to see a similar fall in freight tonnage;

(ii) durable goods spending started to drop since the end of the stimulus checks policy – Loadsmart’s demand for freight tied to this category has visibly drop too;

(iii) continued declines in durables consumption become more likely amidst an economic downturn, which will likely result in a drop in volumes for the freight industry.

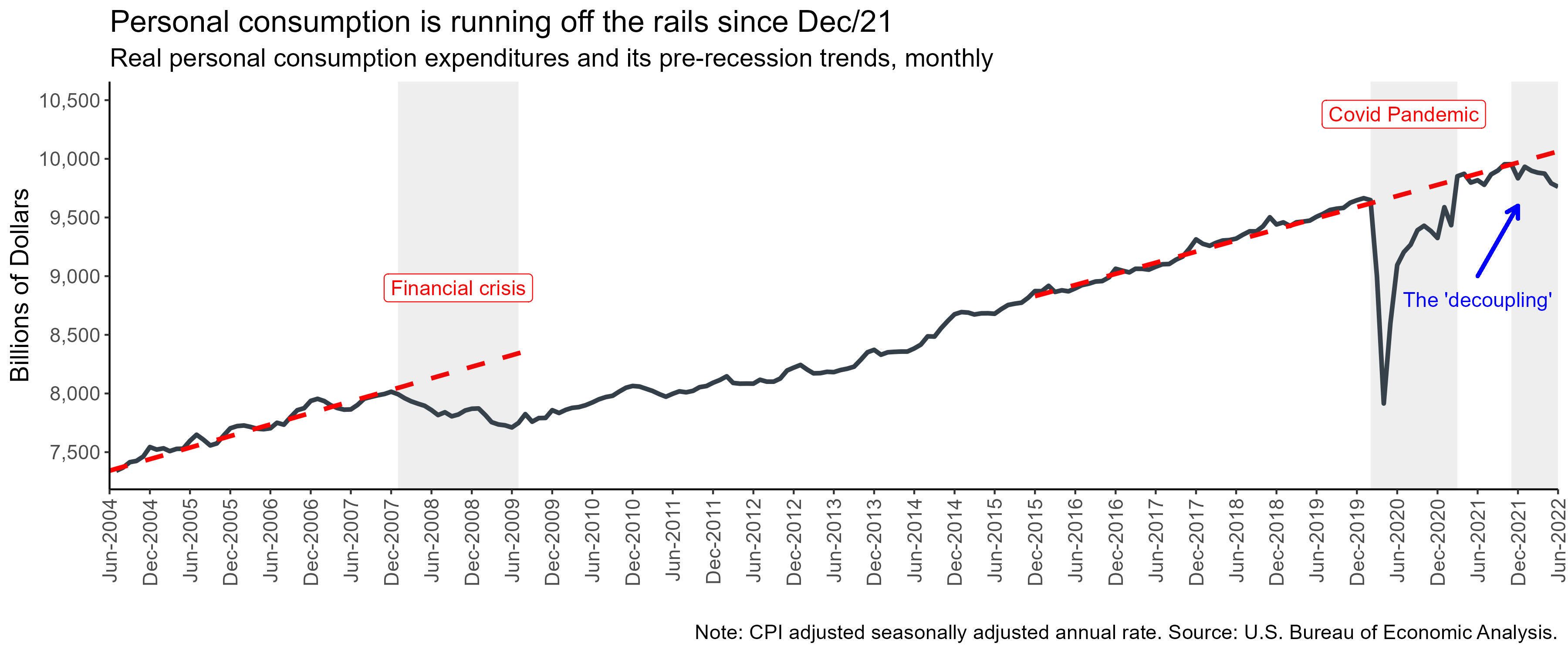

In Dec/21, real personal consumption expenditure started decoupling from its pre-pandemic growth trend – as seen in Figure 1. But this decoupling is still far from being as severe as the one brought by the 2007 financial crisis. Last June, overall consumption maintained its same level YoY, while amid the financial crisis in 2007 it was declining 2% YoY on average every month.

Typically, governments have more tools to fight inflation-driven recessions (e.g. interest rate hikes) than credit-driven ones, but given the geopolitical issues at play (the sanctions against Russian oil, the resurgence of US-China trade war tariffs, etc) the negative economic scenario will likely remain.

Figure 1

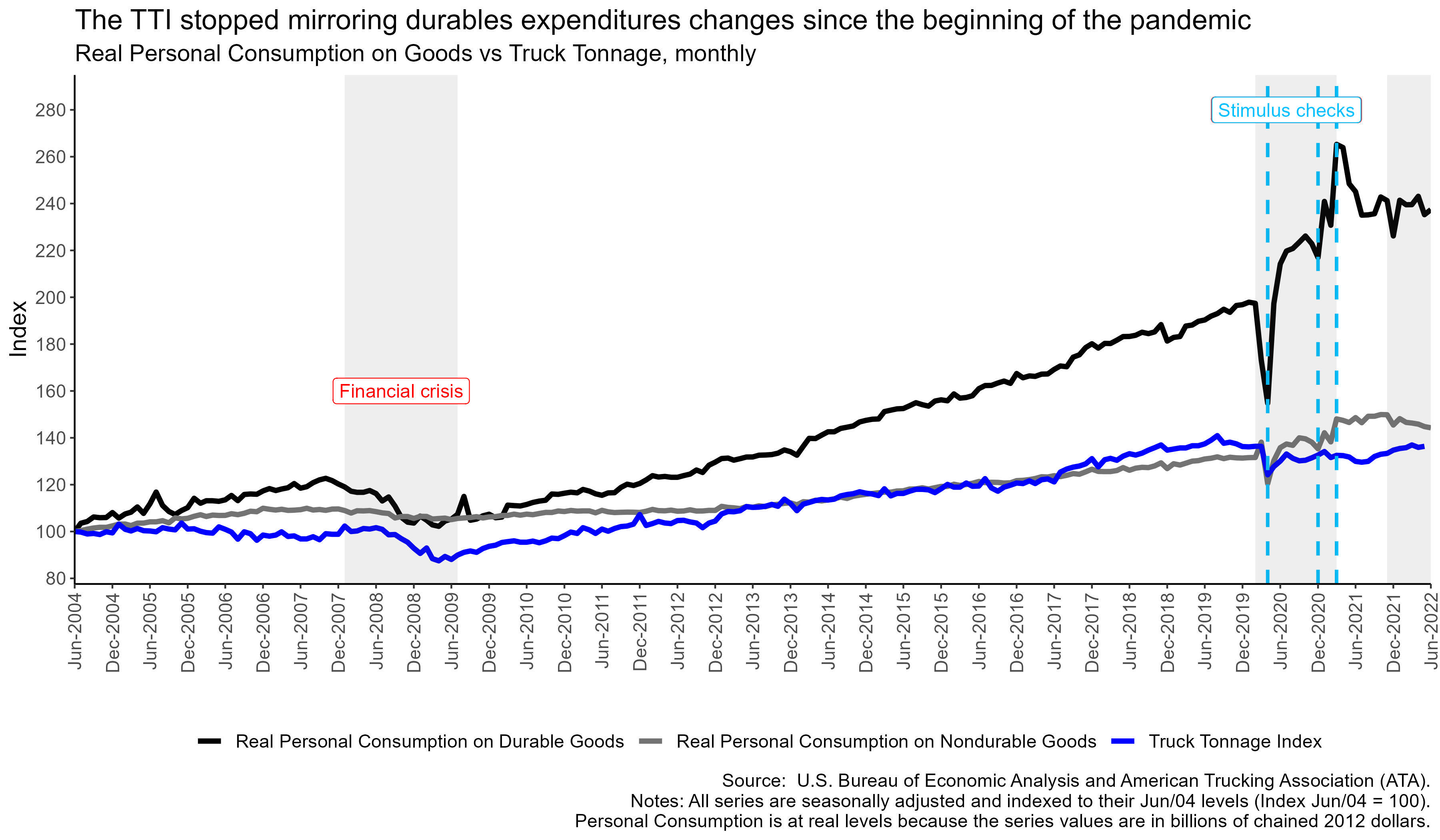

Personal consumption expenditure can be broken down into three components: non-durable goods, durable goods, and services. Although the first two are relevant to the freight world, the second one is the main driver of volatility in the current market.

By connecting consumption spending and the freight market in Figure 2, we see that, during the financial crisis-led recession, the expenditure on goods dropped 10% compared to pre-crisis levels while the tonnage of freight transported by trucks, measured by ATA’s Truck Tonnage Index (TTI), declined 15% in the same period (Jan/08 vs Jun/09).

Figure 2

In the last few years, it was only in the first month of the pandemic (Apr/20) that the TTI had a significant decline (10% MoM) – from which it never fully recovered. The spikes in durable goods consumption triggered by stimulus checks releases had little impact on the TTI. And so did the further decline in durable goods consumption that followed the end of this policy on Mar/21.

In the last few years, it was only in the first month of the pandemic (Apr/20) that the TTI had a significant decline (10% MoM) – from which it never fully recovered. The spikes in durable goods consumption triggered by stimulus checks releases had little impact on the TTI. And so did the further decline in durable goods consumption that followed the end of this policy on Mar/21.

One hypothesis as to why the TTI stopped moving in line with durable goods expenditures is that it became outdated due to its inability to capture spot freight’s share of the market. As shown by Sonar’s OTVI (truckload volume index), tendered truckload volumes increased by 40-50% from 2018/2019 to 2021, while the TTI only shows a minor recovery in tonnage following the pandemic (at lower levels than in 2018-2019). From Q2 2020 to January 2022, the amount of freight moved in the spot trucking market has soared, but the TTI did not seem to mirror this change.

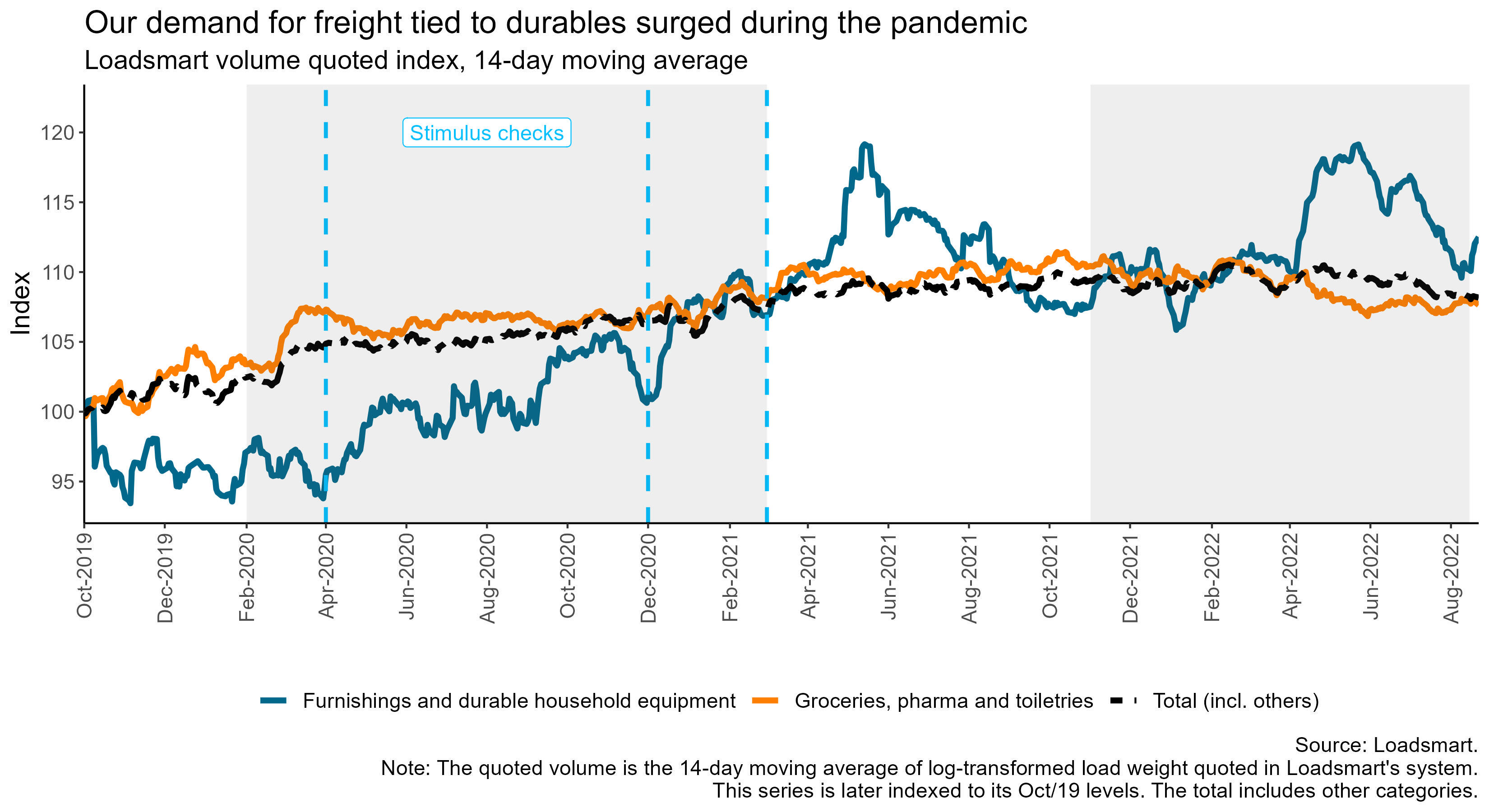

By plotting Loadsmart’s quoted spot volume, we see that, indeed, demand for freight tied to durable goods – proxied by our “Furnishings and durable household equipment” commodity category – surged in tune with the release of the stimulus checks, increasing by 11% during the pandemic (Feb/20 to Mar/21) – as displayed in Figure 3. In the same period, the demand for freight tied to non-durables, represented by “Groceries, pharma and toiletries”, increased only by 5%.

But the reason why our overall quoted volume has not been largely impacted by the drop in durables consumption so far is that the largest chunk of our demand actually comes from moving non-durable goods, the least cyclical component of overall consumption expenditures.

Figure 3

In the current recessive scenario, we expect durable consumption to continue to decline at a faster pace than non durables and services, which should cause notable downward pressures on overall freight tonnage (a pressure that we are currently feeling at Loadsmart). As we all know, further weakening in freight demand will leave trucking businesses to operate with even more capacity which would likely result in further rate declines.

In the current recessive scenario, we expect durable consumption to continue to decline at a faster pace than non durables and services, which should cause notable downward pressures on overall freight tonnage (a pressure that we are currently feeling at Loadsmart). As we all know, further weakening in freight demand will leave trucking businesses to operate with even more capacity which would likely result in further rate declines.