Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market. We hope you enjoy! #movemorewithless

Full Truckload Market Overview

Volumes

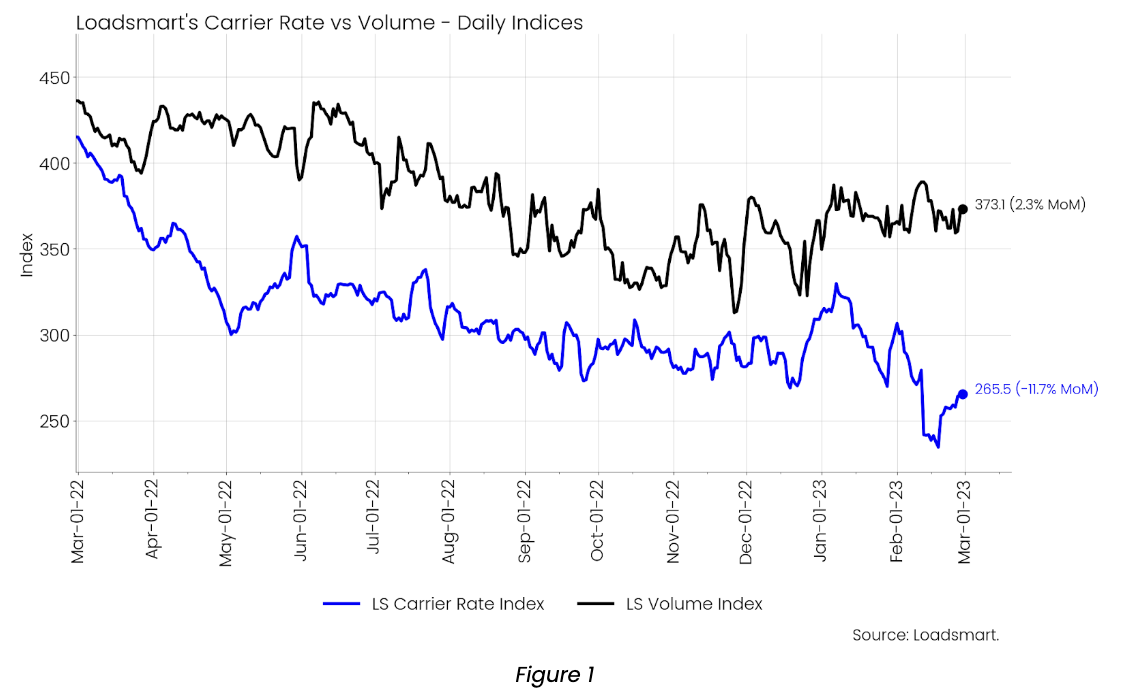

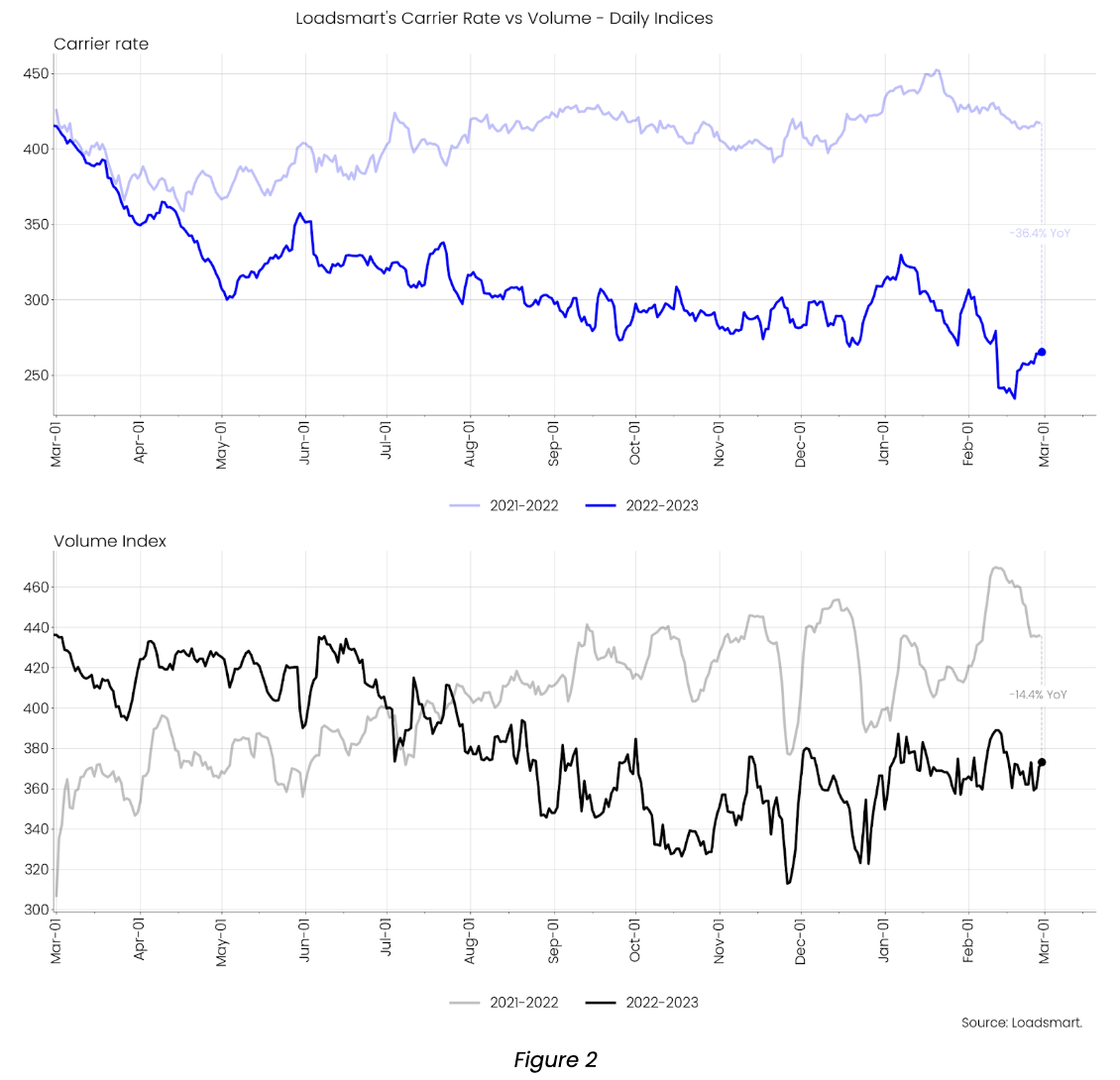

Our volume index increased by 2.3% in February MoM (Jan-31 to Feb-28). The index was rather stable during the month. Despite the fact that we are still in a deflationary trucking market, our volume's performance since Q4’22 has actually been positive. Using the monthly average, the index rose for the fourth consecutive month, resulting in a 10% gain since October 2022.

- This upward trend has been more prominent in the Southeast so far (maybe early signs of produce season?), where the index already increased by 24% since October; followed by the Southwest, Northeast, and West - which all had similar increases of around 15%. The only region where volumes are still near October’s bottom is the Midwest.

Rates

Our price index decreased by 11.7% in February (day 01 to 28). By mid-February, the index reached its lowest point yet in this market cycle. Prices dropped in all regions around the second & third week of the month, but then slowly regained steam in the last week of February.

- Note that we previously forecasted that rates would hit their bottom in Mid-February, however we did not expect them to drop as low as they did (-13% drop vs our forecasted 3-5% drop)

Loadsmart’s Look Ahead:

Something that we’re watching closely over the coming months that we should all be familiar with: will the US economy see a soft landing or a hard fall in terms of recessionary impacts in 2023?- Our view on this has shifted more bearish recently due to continued inflation concerns and resulting contractionary financial policies

- For example, for inflation to ease we would need to see unemployment increase, but the labor market is still tight: (i) the unemployment rate is at 3.4%, the lowest level in 54 years; (ii) wages and salaries were up 0.9% in January.

With the further economic contraction as well as Consumption / Industrial Production slowing, we don’t expect the freight market to begin its rebound until Q4’23.

- That said, it’s good to remember that the freight market can turn inflationary even amidst an economic downturn - if we see substantial amounts of capacity exit the market in Q2, this could rebalance the supply & demand equation and lead to some tightening as early as Q3

Freight & Economics

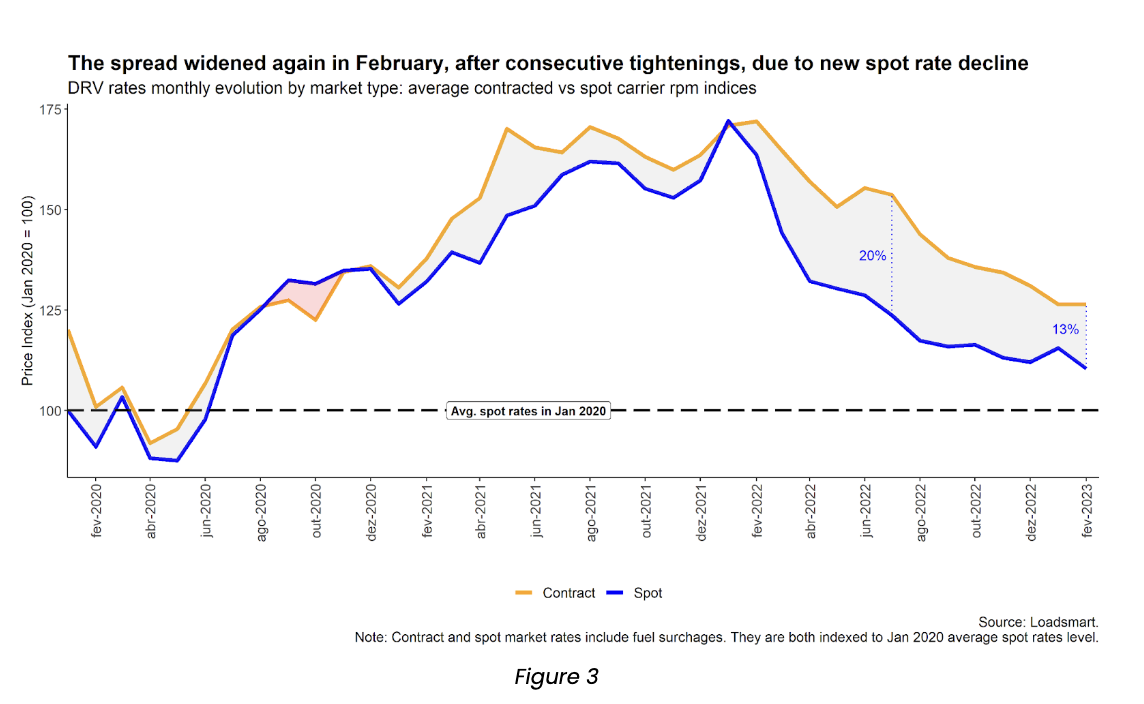

Rerouting to the East:

- The decline in imported goods in Q4 2022 was more pronounced on the West Coast. In addition to weakening domestic consumer demand, the fear of operational disruptions stemming from dockworkers' strikes in the region has led US industries to shift their import activities to the East Coast.

- Figure 4 shows that from October to December, total imports had a sharp decline. But on the West Coast, the downfall started more severely in August 2022. In December, the level of imports in the region was already 23% down from its peak in August of 2022.

The fear of port strikes stems from the fact that over 22,000 dockworkers from main West Coast ports have been working without a contract since July 2022. The bargaining between workers and ports is still ongoing. No strikes have been scheduled so far but negotiations are not open to the media, which creates an atmosphere of uncertainty among importers (check here for the official joint statement from the parties in negotiation).

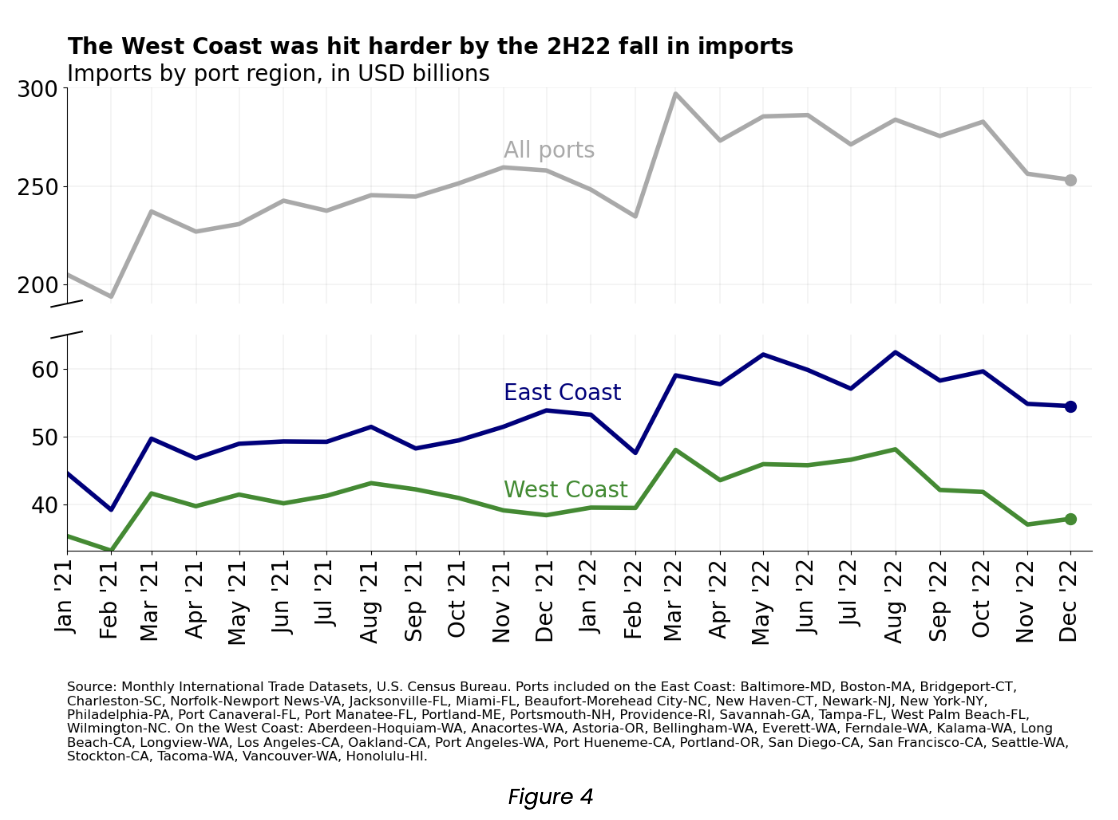

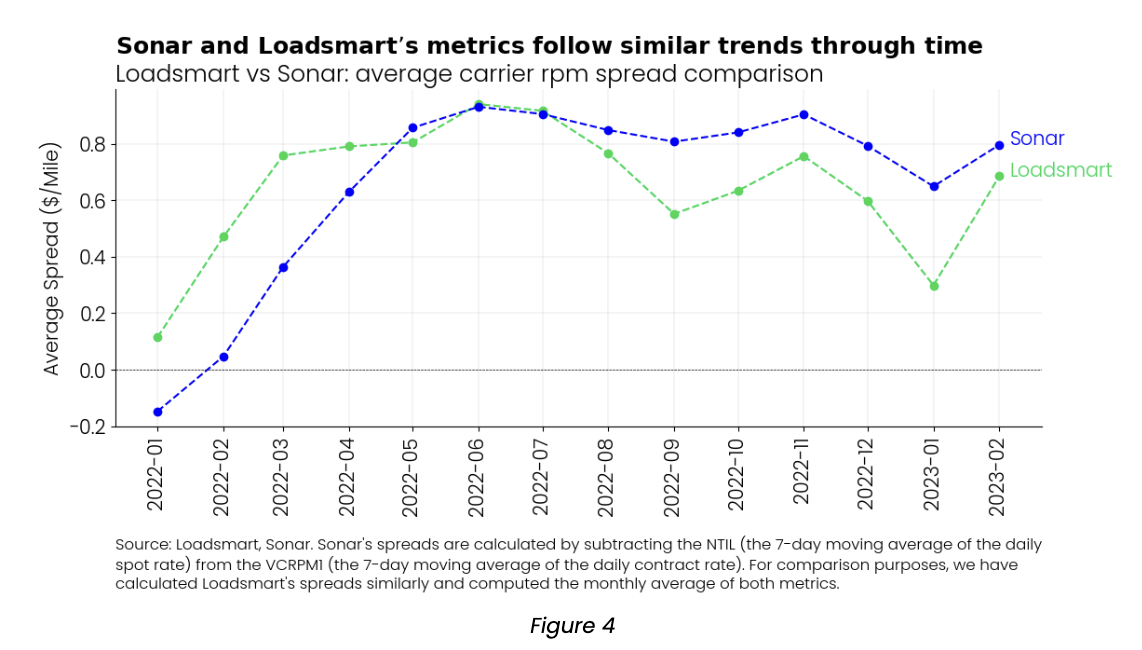

Contract to Spot Spreads:

As we predicted at the end of last year, check out this LinkedIn post from December, the spread between contract and spot rates started the year on a downward trajectory. The reasoning behind our forecast was that shippers would take advantage of the soft freight demand & excess capacity, pushing contract rates down to follow spot levels; carriers, in turn, would keep an effort to maintain minimum contracted volumes in 1H 2023 bidding season.

We are now seeing this trend take shape rapidly: from July 2022 to January 2023, Loadsmart's average monthly spread dropped 10 p.p., from 20% to 9% - Figure 4. However, the additional spot rate contraction in February brought the spread back up to 13%.

- In February, our spot price reached a new floor, while the contract price remained stable at a level similar to January, leading to a widening of the spread. Sonar metrics showed a similar pattern, suggesting that the spot prices slide was widespread in the market.

- Sonar and Loadsmart’s metrics follow similar trends through time, although Loadsmart’s spreads have reached lower levels since the beginning of 2H 2022 - Figure 4.

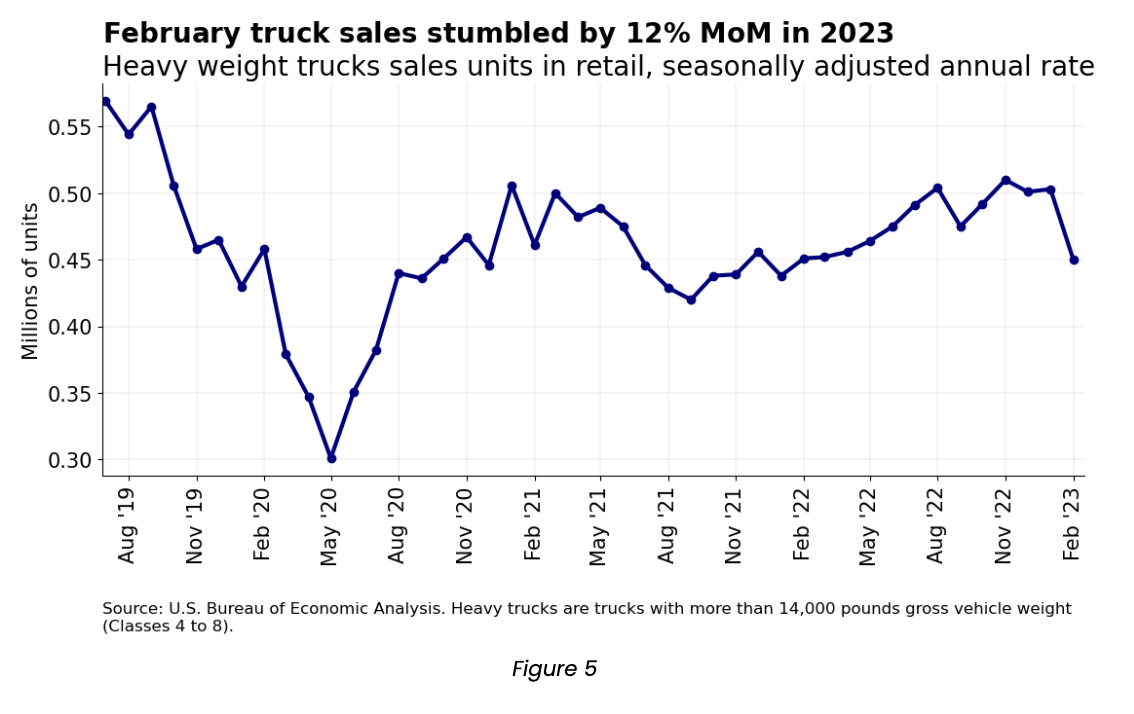

Heavy Truck Sales:

Heavy truck sales are down to 450 thousand units in February, a 12% decline MoM. The biggest monthly decline in sales in over three years - Figure 5.

Despite the recessive freight market during 2022, truck sales continued to rise throughout the year, likely due to the shortage of trucks in inventory during the pandemic period. However, recent data suggest that the late truck replacement cycle that supported the market last year is now over.

In addition to the recessionary scenario for trucking, vehicle financing conditions worsened due to consecutive interest rate hikes in 2022. This will make it harder for truck sales to return to pre-crisis levels this year.

As always, please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you!

---------------------------------------------------

For more about how you can understand the current market to plan for the future, download our quarterly report.