Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless

Loadsmart's 2023 Truckload Market Outlook:

In our view, Q2’23 will represent the spot market bottom, but a notable short-term recovery is unlikely given the current economic environment. We forecast a 10-15% increase in our spot rate index by the end of Q4’23, with a significant spot market recovery coming in 1H’24- According to the data presented in a section below, the arrival of spring should warm up the consumer market. As a result of this and produce season, we expect 2Q2023 to be better or equal to the previous quarter, but definitely worse than 2Q2022.

- Despite the hope for seasonal improvement, the broader macro environment for the freight transportation market will continue to be challenging. The April jobs report signaled that the U.S. labor market remains tight, making it less likely that inflation will ease next month. As a result, consumption of goods may continue to slow down, further delaying excess truckload capacity rebalancing with demand.

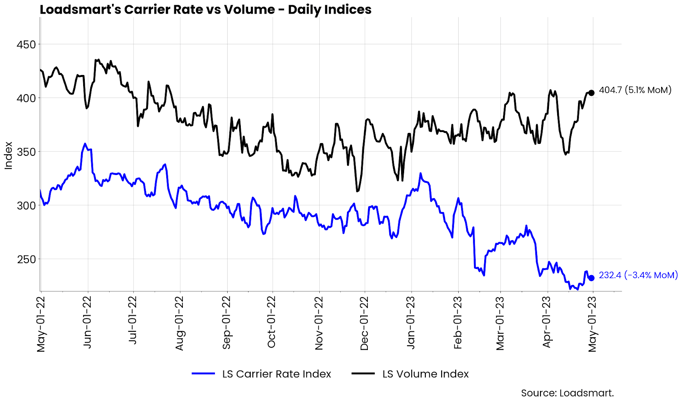

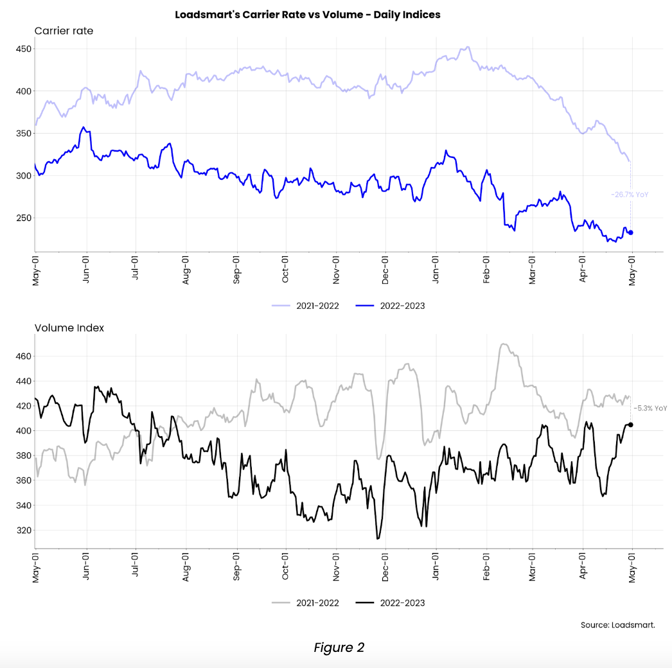

April 2023 Truckload Market Update:

Figure 1

Figure 1

-

- Our year-over-year volume performance continues to be negative but has outpaced the market so far: Sonar's OTVI data is down 16% YoY, while we are down only 5% YoY.

- Rates were down in all regions, except for the Midwest, where they rose 9% MoM. The Midwest region has, in fact, surpassed the traditionally more expensive Northeast region as the nation's highest carrier RPM for the first time this year, which can be an outcome of the growing volumes outbound from the region. Since March, the total volume sourced in the region has grown by 17%.

Freight & Economics Outlook

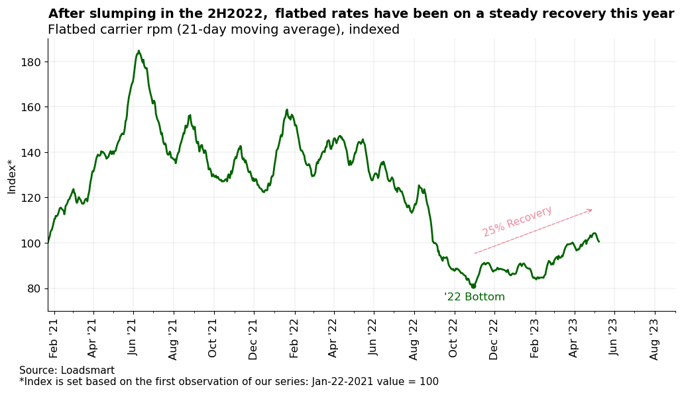

Flatbed Recovery

While there is still uncertainty in the truckload industry as to whether dry van rates have bottomed out, there are reasons to be optimistic about the flatbed share of the market. Loadsmart’s flatbed index started recovering in November ‘22 and is currently 25% up from the ‘22 bottom.

Figure 3

We have reasons to believe flatbed rates will continue upward from November’s bottom because:- Non-residential construction is booming and the uptrend should remain in the next months. U.S. manufacturers are in a re-shoring process, which intensified the demand for commercial and industrial buildings over the last year. The current construction spending expansion is being driven by this.

Manufacturers began re-shoring during the pandemic as they felt the need to regain control of their end-to-end supply chain. However, the re-shoring trend has intensified in the last two years, spurred by U.S. government policies, namely the bipartisan infrastructure bill and the recent CHIPS and Science Act.

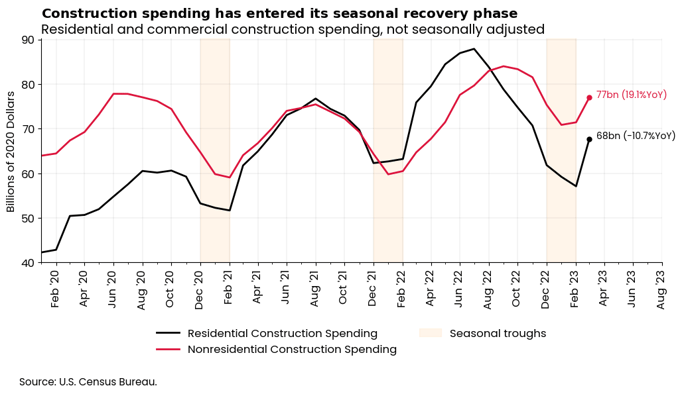

These public initiatives are expected to continue to fuel the construction sector in 2023, driving further spending growth that should leverage flatbed demand. - Seasonal Recovery: The construction sector is characterized by a strong seasonality, with construction booming in the summer and slowing down in the winter. As shown in Figure 4, February is typically when the construction spending cycle troughs and moves into the expansion phase. Hence, we expected the seasonal rebound in construction spending to also boost flatbed rates in the next two quarters.

Figure 4

Figure 4

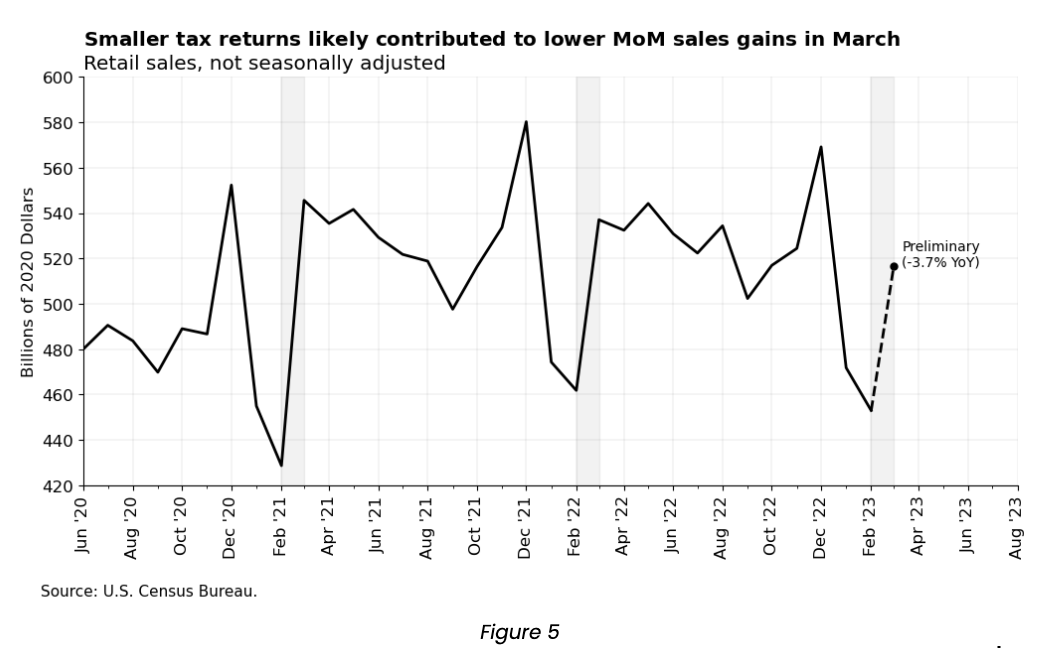

Retailers May Have a Soft Start To Spring

February to March is typically the time of year for retail sales to pick up given the combination of warmer weather and tax refunds. Still, preliminary data from March (in Figure 5) shows that sales growth was not as strong as in previous years.

Retail sales rose 14% MoM, while the average March gain over the past three years was 23%. In addition to the inflationary scenario and underlying economic uncertainty, this year's smaller tax returns - typically released in March - may have contributed to slowing sales in the 1Q.

Weak retail sales will continue to dampen the chances of freight rates picking up in 2Q2023. From a seasonal perspective, we should have a better 2Q than 1Q2023 due to spring and summer, but in the annual balance, the trend is that trade suffers more year-over-year deceleration.

----------------------------------------------------------------------------

For more about how you can understand the current market to plan for the future, download our quarterly report.