Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

June Spot Rate Forecast

Our latest spot rate forecast, predicts a June bottom for truckload spot rates and a minor recovery through Q3-Q4 as we head into peak retail season. As stated previously, our forecast indicates that we shouldn’t expect a hot market (i.e. primary tender rejections >=10% and spot rates up 15-20% YoY) until Q2 2024. Here’s why:

- The FOMC has given indications that reducing interest rates, and therefore stimulating the consumer/economy, is unlikely to happen any time soon

- Excess capacity in the market continues to absorb any potential market catalysts. Lower fuel and large profits from the bull market have enabled carriers to stick around much longer than expected

- Our enterprise truckload shippers have reduced volumes on their 2023 bids on a YoY basis. There of course can be many different factors at play here, but it certainly points toward reduced freight demand in the second half of the year

Unsurprisingly since contract rates tend to follow spot rates with a 1-2 quarter lag. We expect contract rates to come down another 10-15% over the next 4-5 months

May's Full Truckload Market Overview:

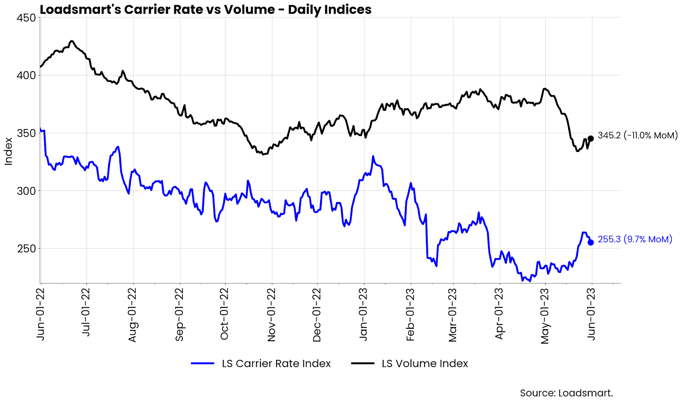

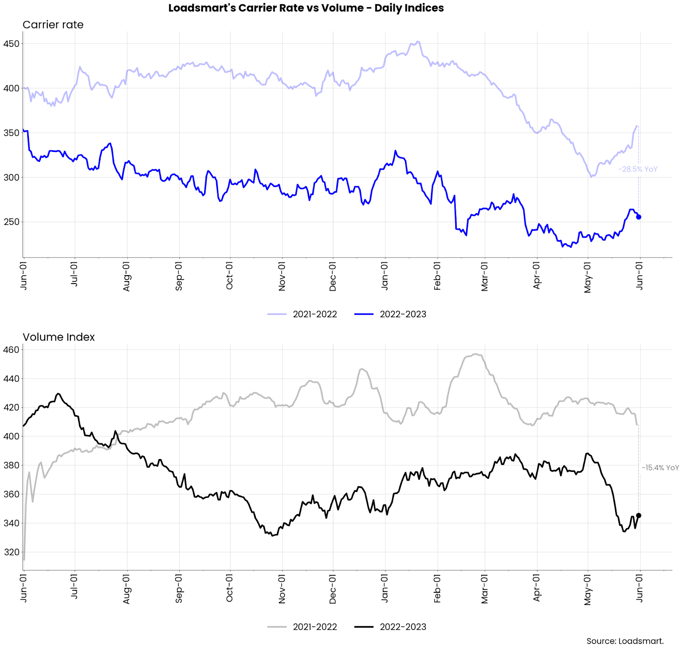

Volumes: Our volumes Index decreased by 11% MoM in May. There was a reversal in the volume growth trend that started in November 2022. From early Nov to the end of May, our index rose 15%, but by mid-May, it plummeted, returning back to November levels.

- The decline in procurement volumes was likely a result of rate increases stemming from minor DOT week & Memorial Day disruptions. Quoted volumes on our platform continued on an upward trend throughout May.

Rates: Our price index increased by 9.7% MoM in May. After the April lows, our prices began a mild upward trend in mid-May, again stemming from DOT week & Memorial Day impacts. However, as rates rose, volumes fell, indicating that there is still excess capacity in the market and that shippers are unwilling to pay higher rates for now.

- The only region unaffected by price sensitivity was the Southeast. Even with higher prices, our volumes in the area continued to grow. This is likely stemming from produce season demand.

Freight & Economics

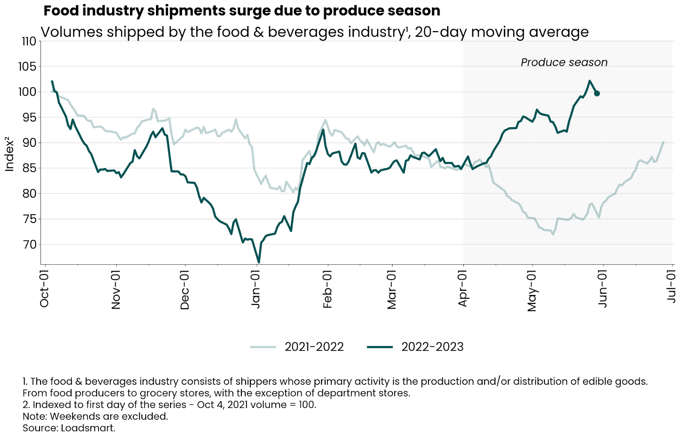

June should see further growth in the food industry's demand for freight

Loadsmart's quoted volumes associated with the food and beverage industry spiked in April and May - as shown below - and the uptrend will likely continue. As we predicted in our Quarterly Report, the volume hike in April was expected to continue throughout the 2Q due to: (i) the production season; and (ii) the fact that the warmer weather leads to an increase in social gatherings, resulting in higher demand for food and beverages.

- The index shown above refers to the demand for all types of equipment. However, when broken down by equipment, the increase in demand for refrigerated trucks was much more pronounced. Reefer quotes from the food & bev industry increased by 40% in May, while dry van quotes increased by around 20%.

- The outlook is positive for June because, so far, the uptrend has been led by the southern regions, but with temperatures rising in more regions across the US, total quoted volumes by this industry should increase further.

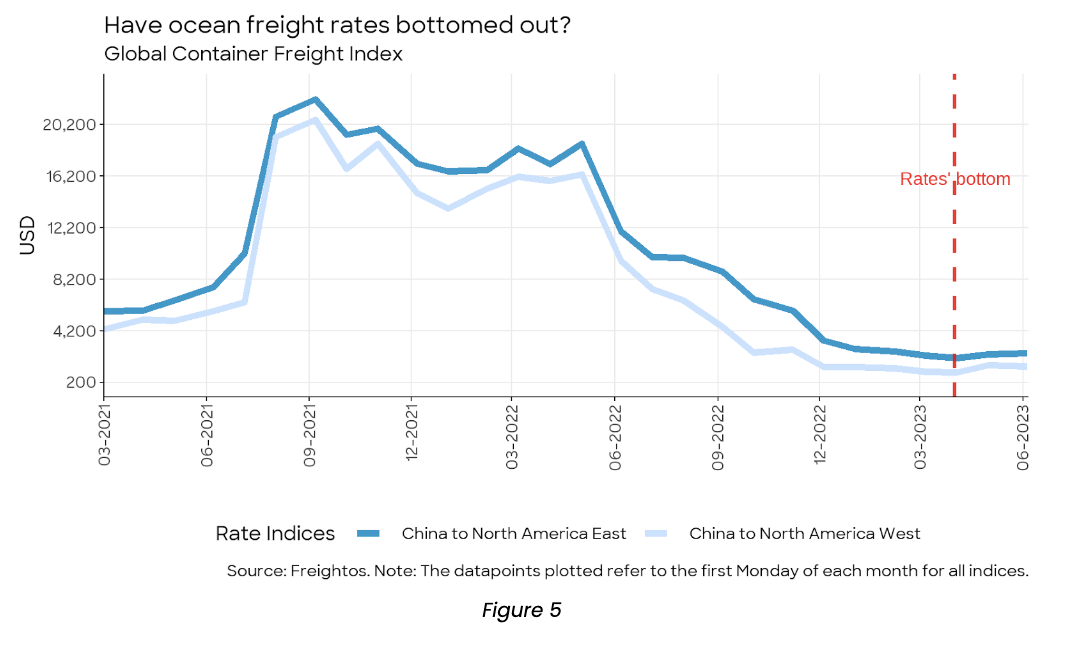

Ocean freight may be heading into a modest peak season this year

Before the Covid-19 supply chain disruption hit the freight industry, ocean shipping typically had a peak season from July through September. As ocean freight rates have bottomed out and stabilized over the past two months, we expect to have this traditional peak back - albeit it will probably be a modest one.- As shown below, US’s most relevant routes reached a floor in April 2023. In that month, rates for containers coming from China to the West Coast and China to the East Coast were around $990 and $2,085, respectively. After that, they both had slight rises and are currently at $1,440 and $2,451.

Now that prices have normalized to levels below the pre-covid period, carriers are ready to test new rate increases as soon as there is a seasonal rise in demand to justify it.

-------------------------------------------------------------------------------------------

For more about how you can understand the current market to plan for the future, download our quarterly report.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless