Share this

As usual, in this Monthly Market Update, we will (a) provide a brief update/analysis of the full truckload market and (b) present a compelling economic analysis to provide a macroeconomic view on the state of the freight market.

We hope you find this report insightful! #movemorewithless

Loadsmart’s top 30 spot rate forecast

Figure 1

Rates: Our price index was up 8.9% MoM in May, with a big swing in the middle of the month driven by the pent-up demand of the May 14-16 DOT week.

- During the first two weeks of the month, prices began a downward trend, reaching YTD lows in key regions. Average prices reached $2.05 per mile in South Carolina, $2.11 in Texas, and $2.20 in Georgia - which drove our index down to 110. The YTD average for these states before May was $2.5.

- A brief rally then began after the 16th, driven by pent-up demand during DOT week. Prices remained high for a few days (~5% above the April average, with the index at 130 versus the April average of 123), but began to return to April levels in the last week.

- Sonar's OTRI jumped from 3.1% on May 1 to 4.3% on May 31. The increase began on May 1 and continued throughout the month, driven by an increase in OTRI in the southern states.

- States such as Florida, Georgia, Texas, and Louisiana all experienced an increase in OTRI of more than 2 pp due to the production season.

- OTRI started the year with an average of 5.3% in January and continued to fall sharply, reaching 3% in April, the lowest level in the last 11 months. It was only in May that we began to see signs of a seasonal recovery.

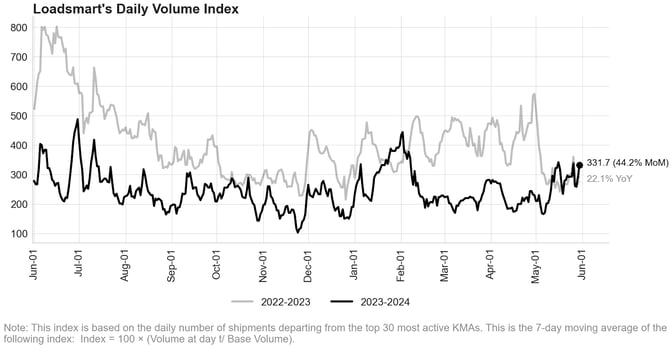

Figure 2

Volumes: Our volume index increased 44.2% MoM in May. The month began with volumes down due to the low freight demand in the Midwest (Illinois, Ohio, and Indiana). But a rebound began after DOT week.

- Much of the demand came from the food, beverages & tobacco, and medical equipment sectors. Freight demand for consumer goods has weakened over the past two months.

- Sonar's OTVI was down 9% MoM. The index rebounded after the second week of the month, similar to our index, peaking around the 26th, but then had a sharp decline on Memorial Day.

Quote rate performance by region

The map shows the average MoM percentage change in quote rate-per-mile for various US Key Market Areas (KMAs).

- Rates are trending lower in about 70% of the KMAs.

- In the Midwest region, low demand has been leading to lower rates since March 2024, and only after the third week of May did we start to see a modest recovery.

- Texas, Louisiana, and Mississippi continue to trend up, given the produce season, but prices cooled down in other Southern regions, such as Florida, Georgia, and Alabama.

- Rates improved in Mountain West regions.

Figure 2

- Rates are expected to improve modestly in the coming months, driven by seasonality. They should end the year with an increase of only ~5-10% from current levels.

- We do not foresee structural changes in the truckload market that would lead to more robust rate increases in the near term. The market is oversupplied with carriers and will remain until about July '25.

- Prices are expected to reach $2.56 in July and $2.63 in December 2024 and continue to rise until March '25, when they peak at $2.66, 31% below the Jan '22 high.

Figure 4

Freight & Economics

Decelerating Retail Sales: A Major Headwind for Trucking Recovery

- Retail sales, excluding auto, were virtually unchanged from March to April (0.2% growth) - as shown in Figure 5. The most significant gains were from electronics (+1.45%) and apparel (+1.62%), while non-store retail had the largest decline (-1.20%).

Figure 5

- Although sales growth is still positive, the slowdown is noticeable: In 2021, retail sales grew by an average of 1.1% per month. This growth rate declined to 0.4% per month in 2022 and 0.2% per month in 2023.

- Retail sales growth is expected to weaken further in the coming quarters due to persistently high inflation and slower wage growth.

- Given the slowdown in the retail sector and the diminishing prospects for a recovery in manufacturing activity, trucking demand is likely to remain soft for the remainder of the year.

Trucking Employment: Seasonal Gains But Persistent Year-Over-Year Declines

- Trucking employment increased in April, adding 7,400 jobs to the sector. This increase is consistent with seasonal trends in the industry, where employment typically declines in January and February before rebounding in March and April due to summer hirings.

- Nonetheless, the job gains in April and March were insufficient to produce a year-over-year increase in employment, which is currently down 1.35%, as shown in Figure 6.

Figure 6

- Employment in the sector began a downward trend in June last year and accelerated in August due to the large layoff and subsequent bankruptcy of Yellow.

- Employment was down by 2.8% YoY In August 2023 and continued to fall by 2% YoY on average per month throughout the 2H2023 - exacerbated by the slowdown in the trucking market.

- Employment will likely remain in the YoY contraction zone through at least August 2024 and possibly beyond if rates do not improve. This year's continued contraction in the truckload market is expected to lead to further layoffs.

Questions? Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com).