Share this

In this Monthly Market Update, we will (a) provide a brief update/analysis of the full truckload market and (b) present a compelling economic analysis to provide a macroeconomic view of the state of the freight market.

Full Truckload Market Overview

Loadsmart’s top 30 spot rate forecast

Figure 1

Rates: Our price index rose 19.17% MoM in August. Atypically, this year's Labor Day holiday led rates to spike as some areas of the country experienced capacity tightness. As shown in Figure 2, Labor Day is not historically known for causing price spikes.

- According to Sonar, Labor Day had little impact on tender rejections, the OTRI only increased from 4.3% to 4.8% during the holiday week.

- The average OTRI decreased 0.8 percentage points from 5.3% in July to 4.5% in August.

Figure 2

Figure 3

Volumes: Our volume index rose 20.1% MoM in August. Our volumes spiked in the last week of August due to pre-holiday demand.

- Despite daily oscillations, on average, our shipped volumes have been trending upward in Q3 due to an increase in demand for consumer goods.

- Meanwhile, Sonar's OTVI remained flat MoM and showed a modest increase of approximately 2% YoY, suggesting a more stagnant trend moving into Q4.

Quote rate performance by region

The map shows the average MoM percentage change in quote rate-per-mile for various US Key Market Areas (KMAs).

- Prices in the South cooled in August, dropping approximately 6% MoM, with most KMAs experiencing slight rate declines.

- In the West, rates are trending downward as they declined in most California KMAs, where quotes are generally concentrated, but Washington and Oregon saw moderate rate increases.

- The Midwest also shows mixed trends, but parts of Minnesota and Missouri experienced rate decreases and average quote rate points to price stagnation.

- The Northeast is the only region with an upward trend, likely driven by the KMAs in states such as New York and Pennsylvania showing positive rate changes.

Figure 4

Figure 5

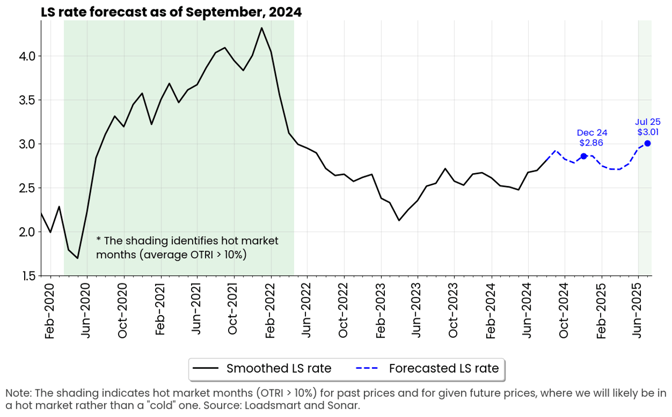

Loadsmart’s spot rate forecast / look ahead

Our model predicts that spot prices will rise from $2.81 in August to $2.93 in September, which should be the peak price in 2024.

- After September, prices are expected to stabilize and remain at ~$2.8 in Q4.

- From a macroeconomic standpoint, there is no demand catalyst to drive a sustained long-term uptrend. Consequently, our projections continue to interpret the recent rate increases as seasonal.

- The steady increase in the volume of consumer goods shipped during July and August, which has driven rates higher, supports the theory that we could be experiencing a peak season pull-ahead, similar to last year.

- Consequently, rate behavior is expected to closely follow last year’s pattern, when prices peaked in September before declining by 2-5% in the Q4.

Figure 6

Freight & Economics

Import activity to decline after September

- According to NRF estimates, August likely marked the annual peak in import activity as retailers had ramped up shipments in anticipation of a potential strike at East and Gulf Coast ports this fall - see Figure 7.

Figure 7

- The contract between the maritime union and the East and Gulf Coast ports expires on September 30. With negotiations currently stalled, a strike could begin in October if a new agreement is not reached by then.

- Importers are expected to shift their cargo to the West Coast in the next months as a precaution against potential labor disruptions, which will further increase the volume of imports at these ports.

- In July, the volume of imports received by the ports of Los Angeles/Long Beach jumped 40% YoY, while for the ports of New York/New Jersey the difference was only 11% YoY - Figure 8.

Figure 8

- For truckers, this means: (1) a potential slowdown in import-driven demand in Q, as import levels are expected to decline and remain similar to last year, and (2) the shift in coastal activity due to strike concerns may result in higher demand for over-the-road transportation from Southern California ports.

- Rates in the Los Angeles/Long Beach key market areas (KMAs) reached a YTD high in August, with an average all-in spot rate of $3.20 per mile - despite the general slowdown in rates across California (see Figure 9). Meanwhile, spot rates at the ports of New York/New Jersey and Houston are approximately 8% below their YTD highs - which occurred in the Q1.

Figure 9

Retailers

- U.S. Census data show that retailers' restocking activity intensified in Q2, leading to an increase in their inventories to sales of about 3% YoY, adding to the evidence that the recent surge in container imports was likely aimed at restocking rather than reflecting a genuine increase in consumer demand.

Figure 10

- In contrast, manufacturers and wholesalers maintained relatively stable inventory levels YoY, with their inventory-to-sales ratio dropping by about 2% YoY.

- From our brokerage perspective, the restocking trend was notable in Q3 as retail demand - particularly from consumer goods companies - was the main driver of our spot volume growth.

-------------------------------------------------------------------------------------------

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. #movemorewithless