Share this

by jpallmerine

Will the gloomy freight market experience any holiday tightening? Potential Q4 price impacts from peak retail season.

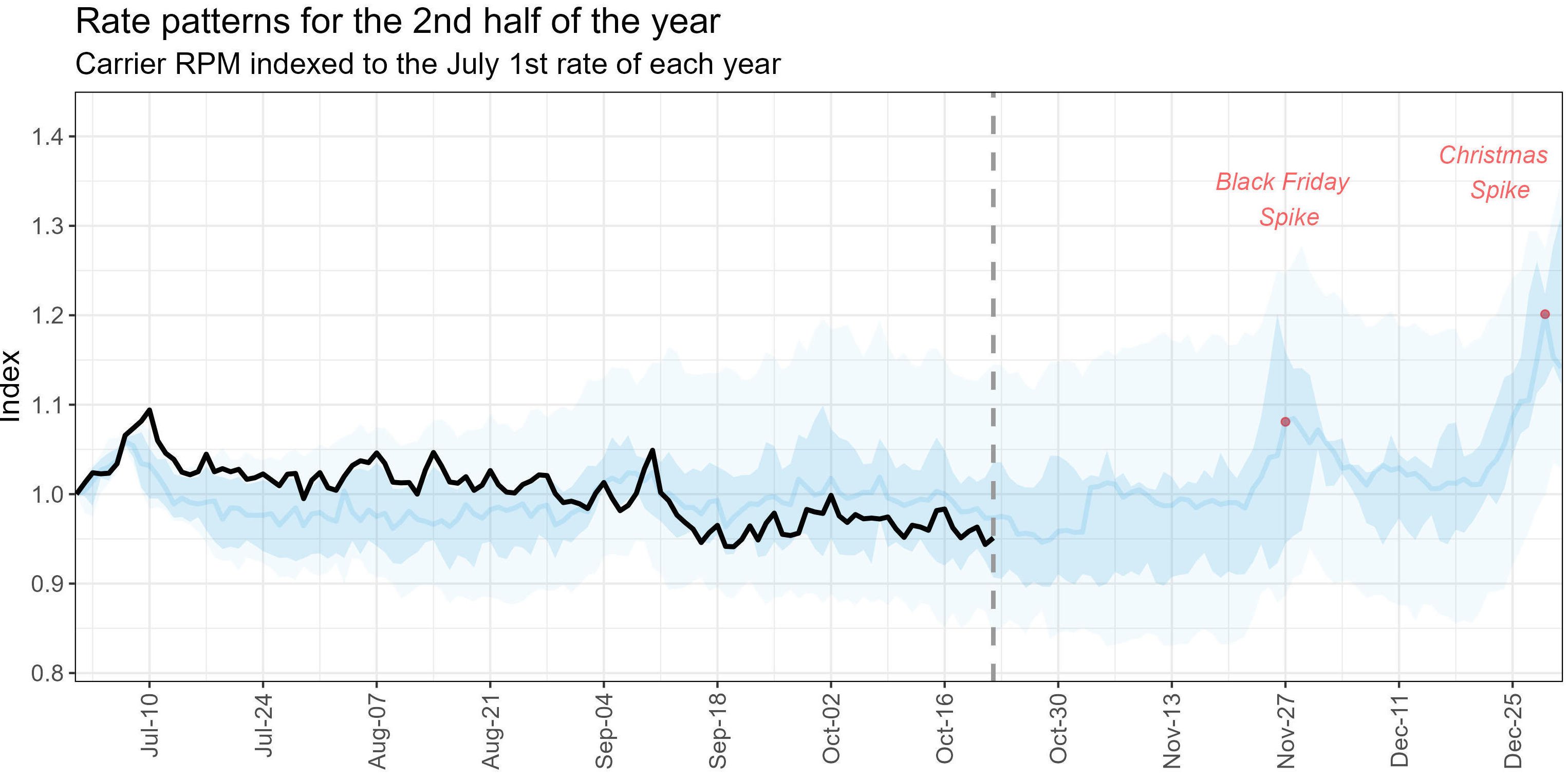

As the holiday season approaches, retail sales performance comes under close watch as a core element capable of providing a lift to the increasingly gloomy freight market. Thanksgiving/Black Friday and Christmas shopping sprees have historically driven market shifts for carrier rates for the last five years. The consumer spending boosts & tightened capacity surrounding the two holidays have historically contributed to a median spike in carrier rates by 10% and 20%, respectively, when compared to Q3 prices – Figure 1.

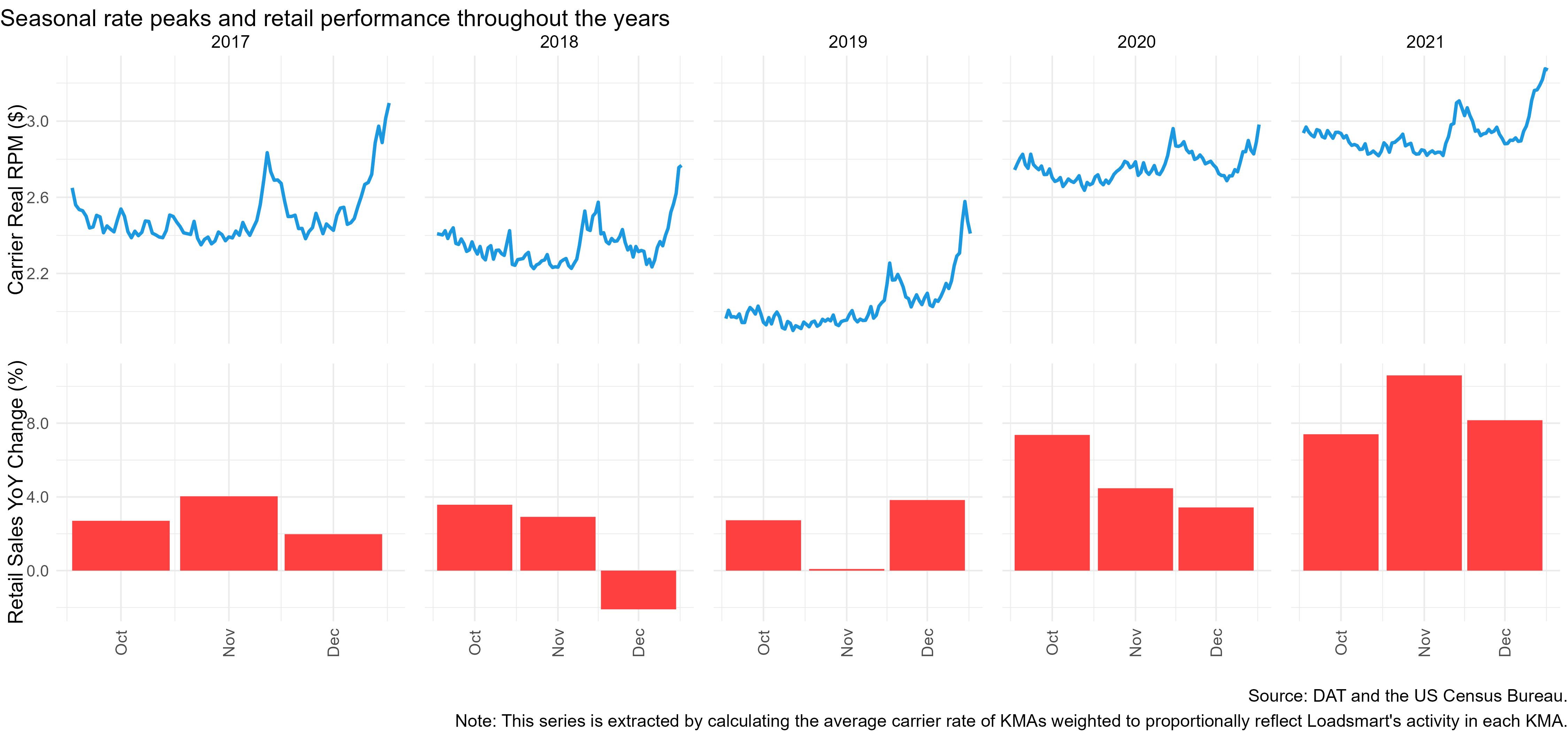

Since 2017, rates have temporarily gained momentum during the fourth quarter even when retail sales growth was weak, as Figure 2 shows, due to tightened capacity. But after the pandemic, seasonal rate volatility began fading because, even amid the exceptional performance of retail in 2020 and 2021, freight price bumps were modest compared to past years. This is possibly due to (i) significant amounts of capacity entering to compete in the hot market and/or (ii) prices were already too high to begin with.

It’s hard to guess at a glance whether there will be any seasonal rate peaks during this year’s holiday season. Firstly because from 2017-2021, there was no generalized recessive scenario that shadowed the entire fourth quarter (as we may have today) and, apart from the COVID-19 outbreak period (Mar to May/20), retail sales dips were sporadic and detached from any lasting trend. Secondly, shippers are well aware of their market position in the driver’s seat which will enable them to mitigate typical seasonal cost increases (the excess capacity in the market easily absorbed the Hurricane Ian disruption, for example).

Under this unprecedented scenario, we attempt to forecast carrier rate’s evolution for the next months using more sophisticated techniques with the goal of understanding how Q4 retail sales performance (either positive or negative) will impact the freight market. The forecast is done considering three possible scenarios for retail sales in the next three months:

- Negative: decline 2.5% YoY;

- Neutral: remain stable – 0% YoY change;

- Positive: increase 2.5 % YoY.

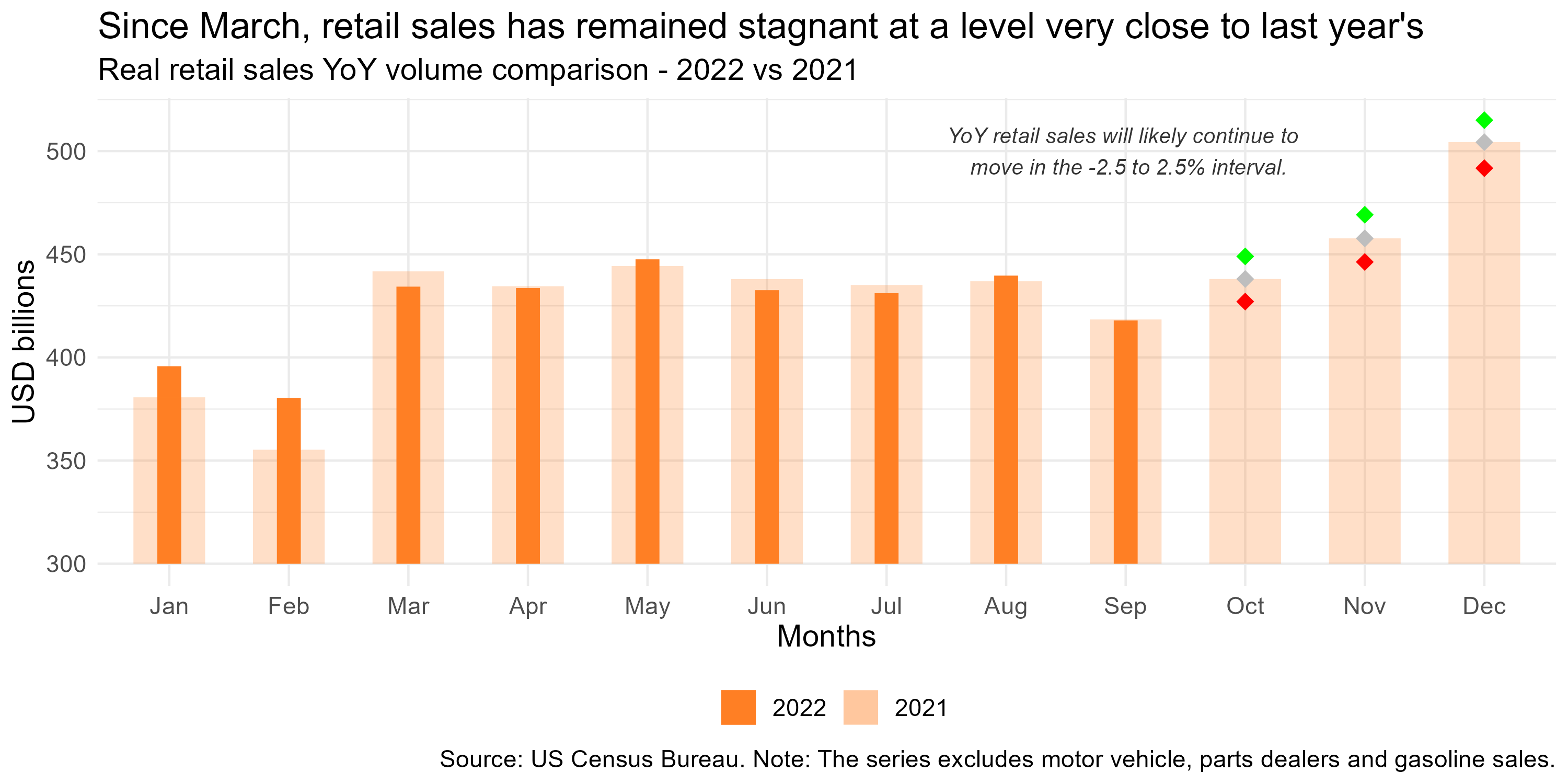

We have arbitrarily chosen this interval for retail sales movement to help us understand the causal effect of it on rates. But given that the average retail sales YoY growth since March is -0.5%, we believe that next months’ rates will likely be within the simulated interval – Figure 3.

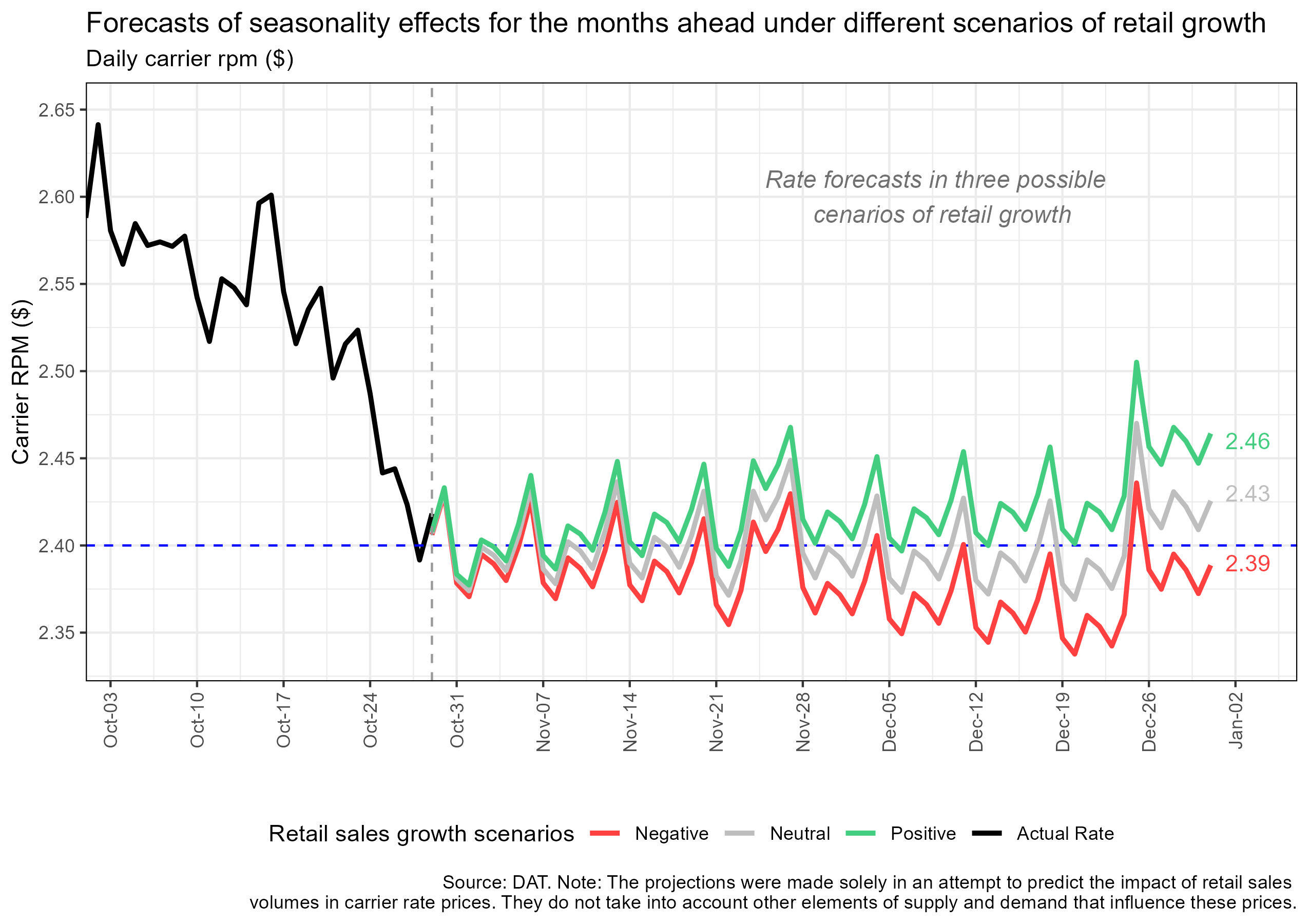

The rate predictions based on the retail sales scenarios are displayed in Figure 4. Based on our estimates, holiday seasonal effects would start kicking in only after Nov’ 22nd. The Black Friday bump should occur from Nov’ 23th to Dec’ 4th and the Christmas bump should begin on Dec’ 22nd.

In a negative or neutral scenario, the downtrend would last through November, ceasing during the Black Friday bump period but resuming shortly after. Rates would bottom on December 20th, in time for the Christmas peak. In a positive scenario, we would reach the yearly bottom by the beginning of November; and, after the first bump, the market would stabilize at $2.4 levels till the Christmas peak.

In closing, it’s important to emphasize that this article is solely focused on studying the impact that retail sales movements could have on truckload pricing in the Q4 peak season. The study is performed based on historical data analysis and therefore intentionally ignores additional factors that could influence freight supply and demand this year.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) or Jon Payne (jonathan.payne@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you!