Share this

As usual, in this Monthly Market Update, we will (a) provide a brief update/analysis of the full truckload market and (b) present compelling economic analysis to provide a macroeconomic view on the state of the freight market.

We hope you enjoy! #movemorewithless

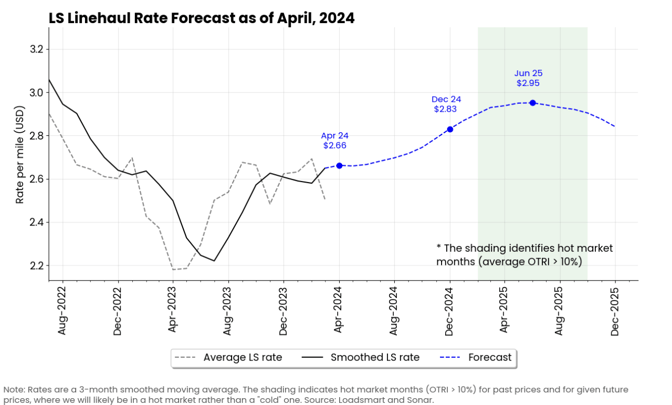

Loadsmart’s top 30 spot rate forecast

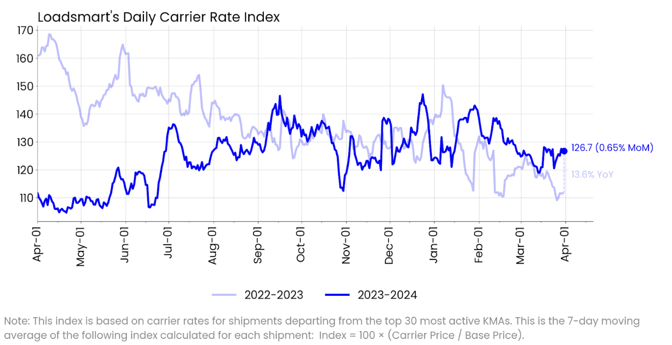

Figure 1

Rates: Our price index rose 0.65% MoM in March, staying almost constant throughout the month. Rates dropped about 20% from mid-January to mid-March. The market then found a new bottom - 5% higher than the Oct'23 one - as the price index hovered around 120 for the rest of the month.- Rates fluctuated by less than 10 cents in most states, which suggests that, while capacity is loose, prices may not fall further in the short term. The exceptions were Florida and Texas, where rates rose more than 20 cents - possibly as an early effect of the produce season

- Sonar's OTRI behaved similarly to our price index but with a two-week lag. From February to March, the rejection rate dropped significantly to roughly last year's level, from 5.4% to 3.4%.

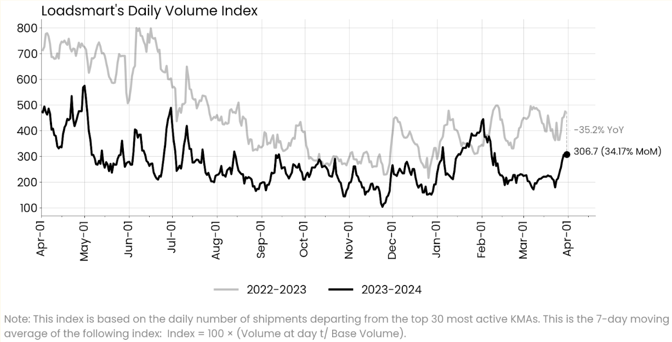

Figure 2

Volumes: Our volume index increased 34.2% MoM in March. Volumes declined from February to early March and remained flat throughout March. However, on the 26th, they rebounded due to increased loads in Texas and Indiana.

- Consumer goods and general retail volumes increased, while food and beverage volumes declined

- Sonar's OTVI declined 7% MoM. The index also remained stable during the month, but unlike our index, it had a sharp drop in the last few days of the month

- Our average rates fell sharply in March, but positive figures in January and February were enough to lift the 3-month smoothed rate

- Monthly average rates have reached a floor for the year. Rates should rise slightly in April as we head into the summer, and freight demand from the food & beverage and construction sectors picks up

- The stagnant behavior of prices since November 2023 shows that the market has failed to fit into the previously projected recovery cycle. We ended 1Q2024 with more evidence that price recovery will be slower than in previous cycles.

- Prices are expected to reach $2.83 by December 2024 and continue to rise until June 2025, peaking at $2.95.

Figure 3

Freight & Economics

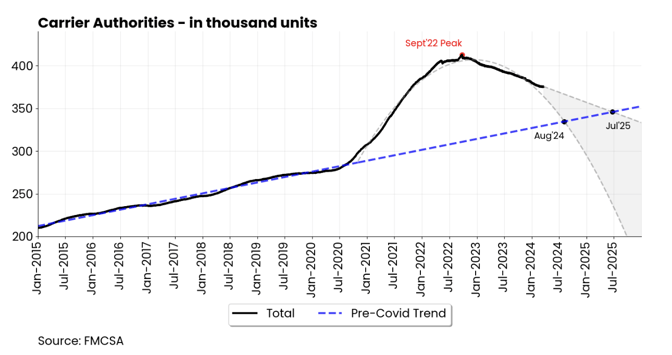

Carrier oversupply may not be fixed until 2025

- The excess of carriers that entered the market from 2020 to 2022 is enduring through its downturn. Until recently, we expected the number of active carriers to return to pre-pandemic levels by August 2024.

- However, carrier exits slowed down in 1Q2024, likely influenced by a brief recovery in rates during 2H2023. We now expect this adjustment process to continue until July '25—see Figure 4.

Figure 4

- Using a representative sample of companies whose information remains accessible on the FMCSA's Safer portal, we identified the profiles of companies that have exited the market and those still navigating through the recession.

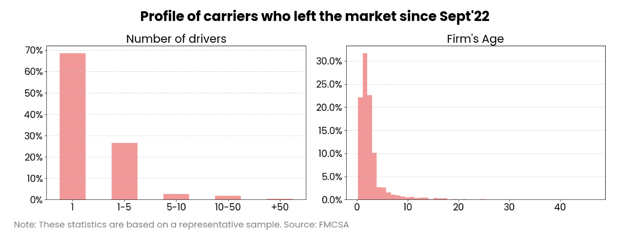

- Companies that have exited the market are younger; 53% had been in business for less than two years, meaning they entered the market after the onset of the pandemic in 2020 - Figure 5.

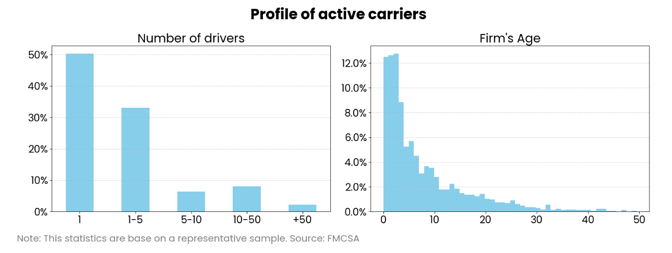

- Also, about 70% of them were owner-operators, while only 50% of those who stayed were owner-operators - Figure 6.

Figure 5

Figure 5

Figure 6

Favorable Market Trends for Flatbed

- As we enter 2Q2024, the flatbed market continues to rally, clearly diverging from the performance of the dry van market.

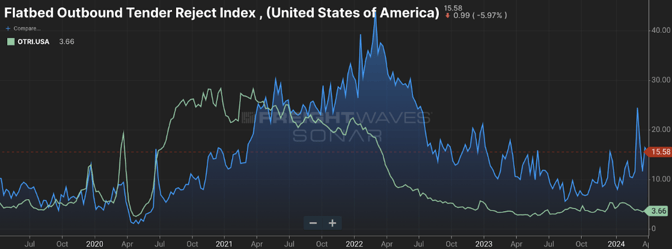

- Both markets bottomed in 2H2023, with flatbed rejection rates at 2.8% and dry van rates at 5%, respectively, and then entered a recovery phase. However, dry van rejection rates declined after Feb'24—see Figure 7.

Figure 7

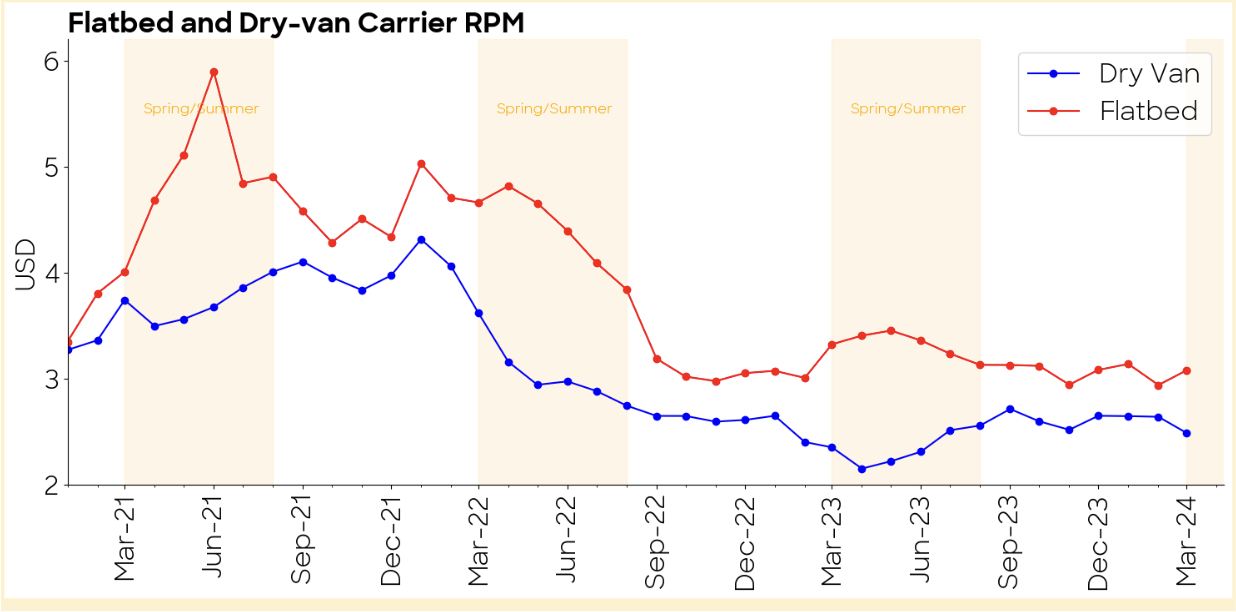

- Based on the current rejection numbers, we are projecting an increase in flatbed rates for the upcoming spring/summer season, consistent with last year's trends. Figure 8 shows that rates escalated to an average of $3.27 in the spring/summer period, in contrast to $3.06, which was the average for the rest of the year.

Figure 8

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you!