Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

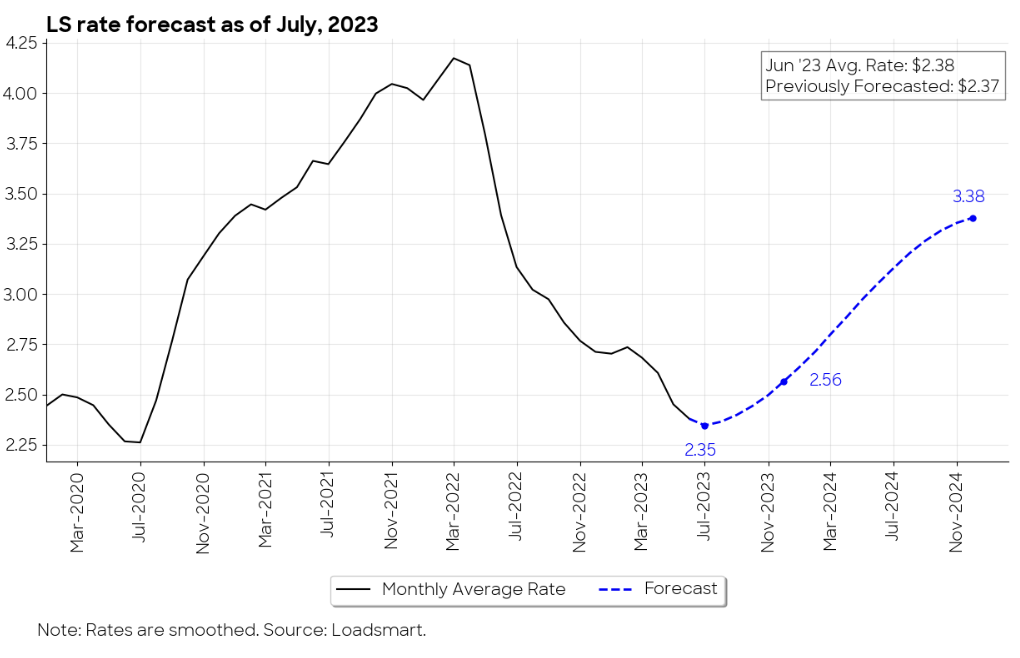

Long-Term Spot Rate Forecast

In this month's publication, we're happy to add a new section to our Monthly Market Update. We are now publishing Loadsmart's long-term spot rate forecast - shown in Figure 3 below. The results are derived from our predictive model, which combines internal data with key macroeconomic indicators and forecasts.

- As of July 1, 2023, our model predicts that the monthly average spot price should finally bottom out in July, falling from the June average of $2.38 to $2.37 in July only.

- Given the current economic outlook of declining consumption and industrial production, the model forecasts a mild recovery starting in August. This turnaround will be largely driven by the fact that capacity tightening has reached its limit, i.e. enough carriers have exited the market to rebalance supply & demand (stemming from extremely low spot & contract rates and lower overall freight volume).

By the end of 2023, our forecast predicts that rates will rise to $2.56 (a 9% increase from July’s forecasted bottom) and continue on an upward trajectory through 2024.

June's Full Truckload Market Overview:

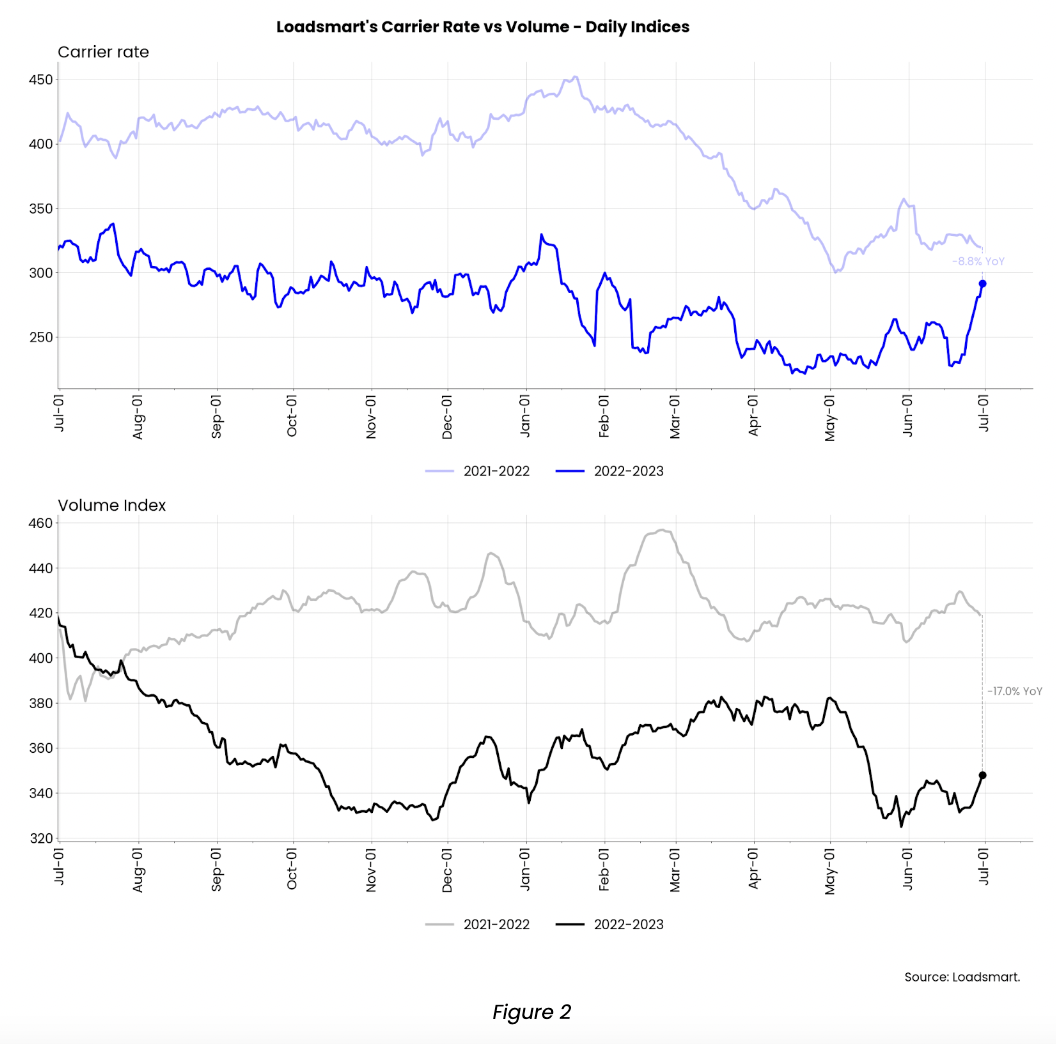

Volumes: Our volumes Index decreased by 4.9% MoM in June. In the first two weeks of June, the index rebounded slightly from its mid-May lows but then it plummeted due to the Juneteenth holiday. After Juneteenth, volumes inched up again.

- In our view, the recent holidays have made our volume data noisy and not very useful for long-term analysis. However, the fact that prices responded so massively to the increase in demand for the 4th of July this year, unlike last year, may indicate that capacity is not as abundant as it once was.

Rates: Our price index increased by 16.5% MoM in June. The index has been on a rather erratic path due to the holidays: prices have had a temporary drop associated with the Juneteenth holiday and a late spike associated with the 4th of July holiday.

- These price fluctuations were greater in the Southwest, West, and Northeast regions, while in other areas they remained stable throughout the month.

- We expect this index to revert back down at least 5-10% as we progress in July, but it should remain above the June lows.

Freight & Economics

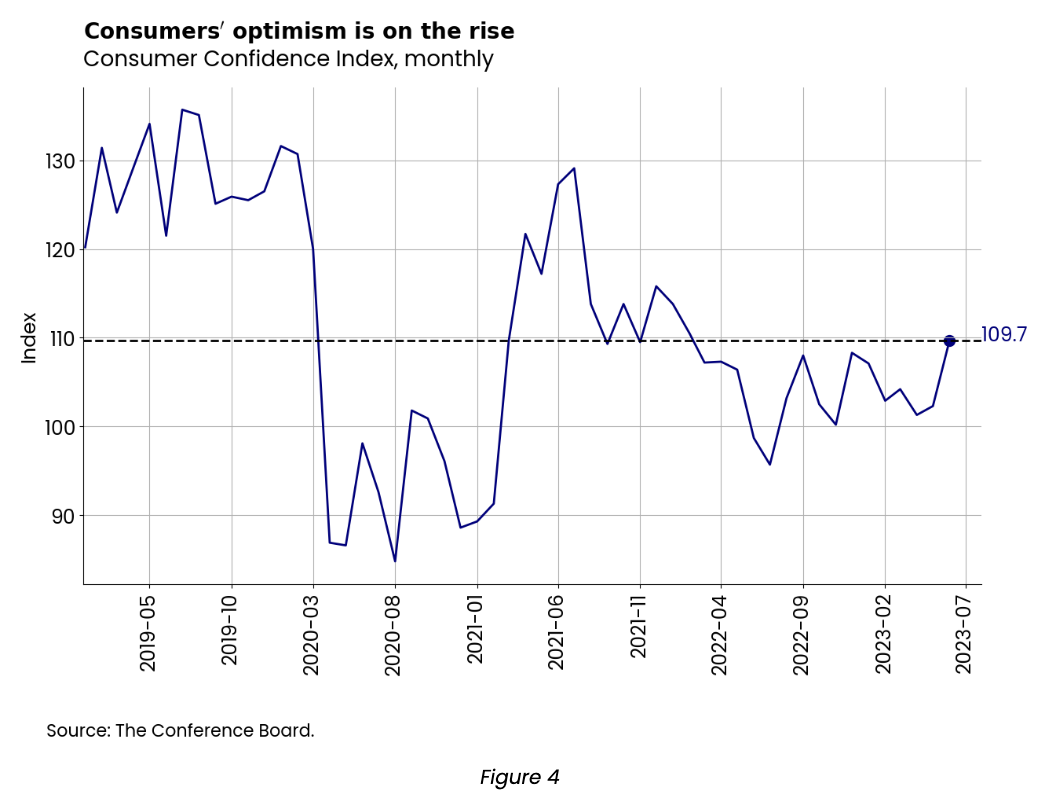

Consumers’ recession fears are fading

The Conference Board's Consumer Confidence Index rose back to levels seen in early 2022 when consumption was still growing above 5% year-over-year. The index jumped from 102.5 to 109.7 from May to June, as seen in Figure 4.

The rise in the index reflects consumers' optimism about current macroeconomic conditions (the labor market, business conditions, and household income), which might be stemming from recent positive news: inflation is easing, the labor market remains strong and the debt ceiling crisis is over.

Consumption data for the months of May and June are not yet available to indicate whether the improvement in the index has translated into a real increase in spending. However, in the current context of economic uncertainty, the rebound in consumer confidence suggests the odds of a soft landing have been raised, at least from consumers’ perspective.

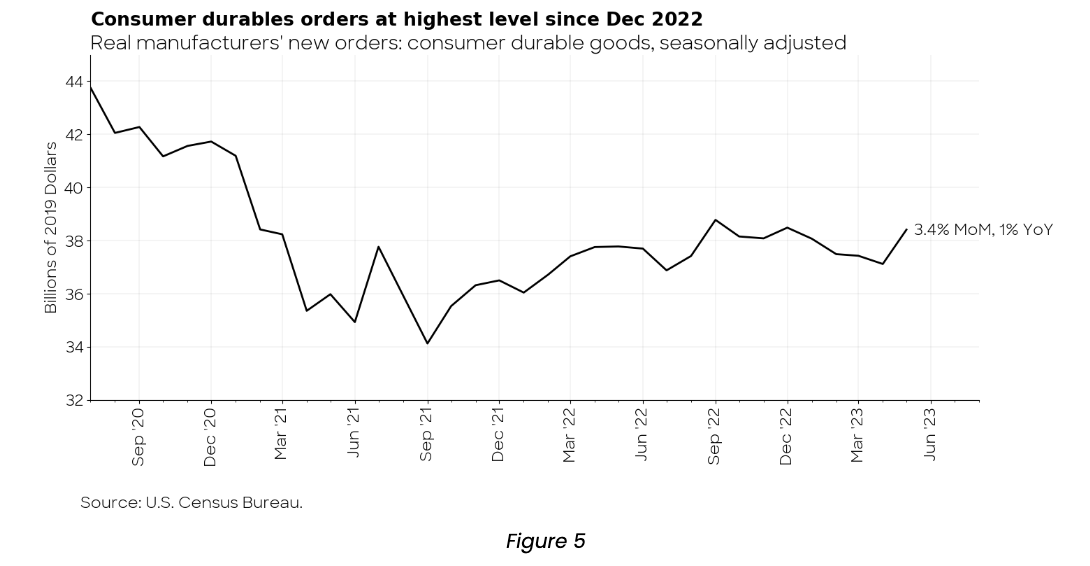

Factory orders are showing strength, although it is limited to a few sectors

May industrial activity results also show signs of resilience. Real consumer durables orders rose 3.4% MoM - Figure 5.

This strength in the factory orders data is mainly driven by motor vehicles, the only sector that has seen consistent order growth throughout the year. The auto industry is one of the few that is still suffering from the effects of pent-up demand due to production shortages during the pandemic.

Household appliance manufacturing orders grew 4% MoM, after consecutive declines since February, and furniture & related products remained stable.

The Manufacturing ISM Report on Business for June also showed an increase of 7% in the New Orders Index, even though the Production index in the month has declined.

In our view, industrial activity associated with durables will remain stagnant, with outputs below 2020 levels until consumer spending responds to an easing of inflation.

-------------------------------------------------------------------------------------------

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless

For more about how you can understand the current market to plan for the future, download our quarterly report.