Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) or Jon Payne (jonathan.payne@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless

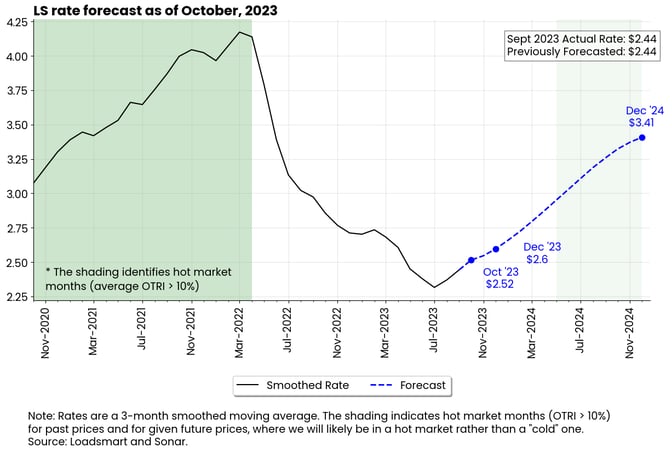

- Since June, when we began publishing Loadsmart's long-term spot rate forecasts, we have adjusted our December 2023 (from $2.56 to $2.6) and December 2024 (from $3.28 to $3.41) predictions due to the mid-year spike in rates, which exceeded our expectations by a few cents in most months, and, most importantly, due to revisions in fuel price expectations.

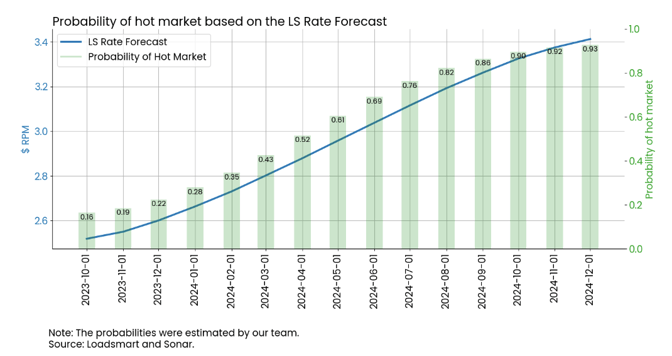

- In Figure 2, we display the probability of being a hot market based on the carrier rate we forecast every month till the end of 2024.

- When LS rates rise above $2.9, the probability that we are in a hot market is higher than the probability that we are not in a hot market.

- Based on these estimates, we are not likely to see a hot market until April 2024.

Figure 1

Figure 2

September's Full Truckload Market Review:

Starting this month, our indices will change. The volume index has been adjusted to reflect more market fluctuations rather than internal volume shifts within our company and, with this change in the volume index, we took the opportunity to rescale our price index using a simpler scale where prices are indexed to the start date of our pricing series (October 1, 2021).

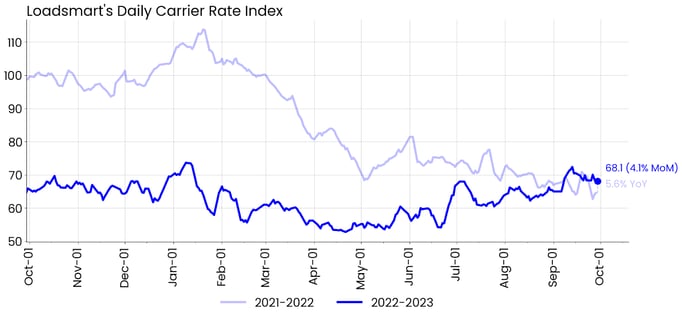

Figure 3

Rates: Our Price Index increased by 4.1% MoM in September. Rates were sluggish at the start due to the Labor Day holiday, but jumped after the second week of the month and continued throughout September at a new level. For the first time in the year, we had a YoY increase in the index.

- Our data was not aligned with the OTRI performance through the month, which fell to 3.6% (from 4.4%) in September.

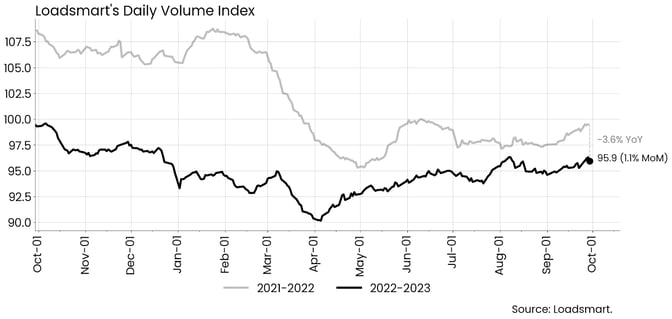

Figure 4

Volumes: Our Volume Index rose 1.1% MoM in September, slightly outperforming Sonar's OTVI, which was flat for the month. The index has already rebounded about 6% from its April low and we expect this trend to continue as we enter the peak season.

Freight & Economics

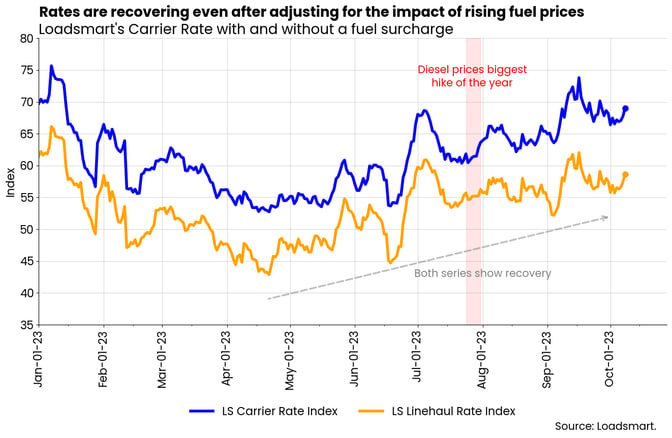

Diesel prices and freight rate recovery

There has been much speculation as to whether the spot rate recovery was simply a pass-through of a diesel price increase to rates. Our data, displayed in Figure 5, contradict this hypothesis.- Firstly, because our rate recovery began in June, about two months before there was a significant surge in fuel prices (diesel prices started an uptrend in July).

- In addition, both linehaul-only and all-in rates have recovered so far. The recovery of the former has indeed slowed due to the increase in fuel prices, but the upward trend continues.

Figure 5

We believe that linehaul-only rates should continue to rise over the long term, even with further fuel price increases, as truck capacity continues to shrink.- According to EIA projections, diesel prices are expected to peak in November 2023 and decline thereafter due to rising oil inventories.

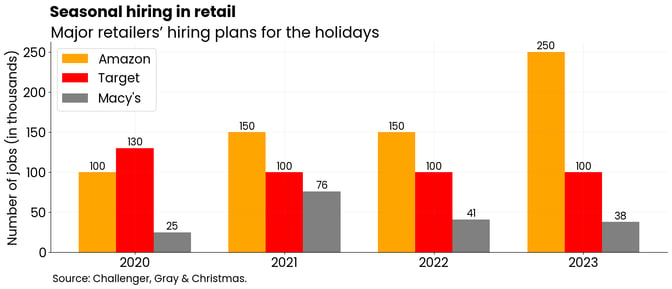

So far, only three major retailers - Amazon, Target, and Macy's - have released their holiday hiring plans. The numbers show how expectations for consumer spending are largely divergent.

- Of the three, Amazon is the only one increasing its numbers from 150k jobs last year to 250k this year. For Target and Macy's, the hiring plans are about the same as they were in 2022 (Figure 6).

Hiring announcements have been mostly muted this year compared to previous years. This may be due to retailers' uncertainty about the state of the economy over the next few months. On one hand, tighter credit availability and the end of the student loan moratorium are expected to weigh on consumer spending in 4Q2023; on the other hand, compared to last year, we have entered the fourth quarter in a better environment with the fall in inflation rates and real income growth.

Figure 6