Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) or Jon Payne (jonathan.payne@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless

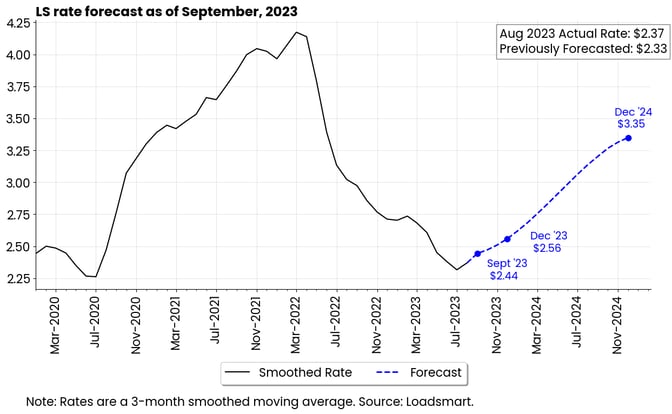

As of September 1, 2023, our model correctly predicted that rates would increase in August, though they increased by $0.04 more than we predicted.

By the end of 2023, our forecast calls for prices to rise to $2.56 (an 8.9% increase from July's low) and continue on an upward trajectory through 2024.

Figure 1

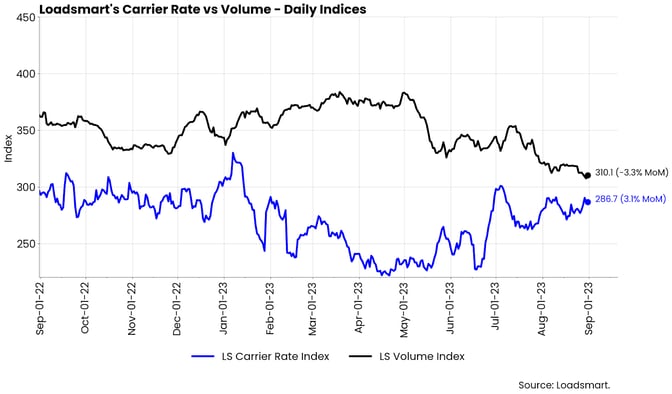

August's Full Truckload Market Review:

Figure 2

Rates: Our price index increased by 3.1% MoM in August, up 25% from May’s/June’s bottom. However, this increase from the bottom is estimated to be closer to +15% if you account for the fact that diesel prices rose by +$0.40 in August.-

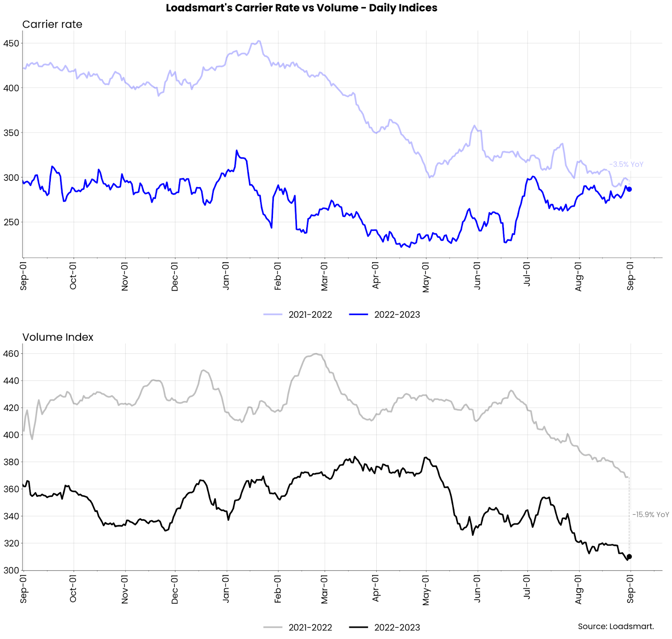

- On a YoY basis (as seen in Figure 3 below), our spot rate index is now only -3.5% YoY, which is the lowest this gap has been since Q1’22. This further supports signs that we are slowly but surely transitioning into an inflationary cycle.

Figure 2

Freight & Economics

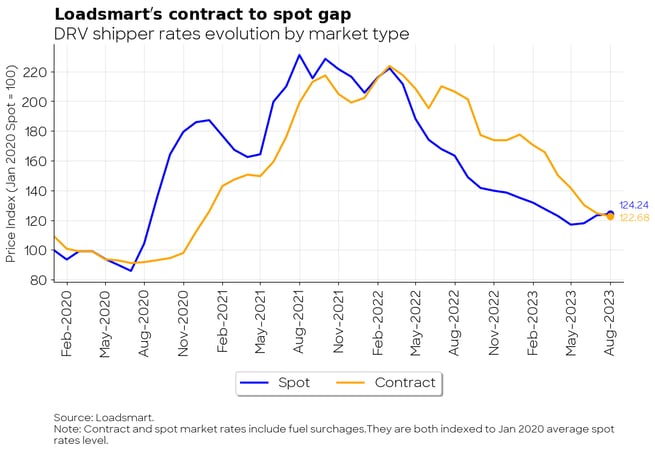

Spot and Contract Rates Converged

The slight recovery in the spot market paired with 7 quarters straight of contract rate reductions have finally brought the two together. Current Loadsmart data, which is not a perfect representation for the rest of the industry which likely has more of a lag, suggests that average spot rates just crossed above the contracts ones for the first time since Q1’22 - as shown in Figure 4.- The difference between the rates in the two markets is minimal for now, but it comes at a key time for negotiations in the contract market as peak RFP season (Q4/Q1) is approaching rapidly.

Figure 4

Typically contract rates lag spot rates by about 6 months, but because the spot rate increases have been so minimal, we don’t anticipate material contract rate increases until Q2’24 at the earliest.Retail sales

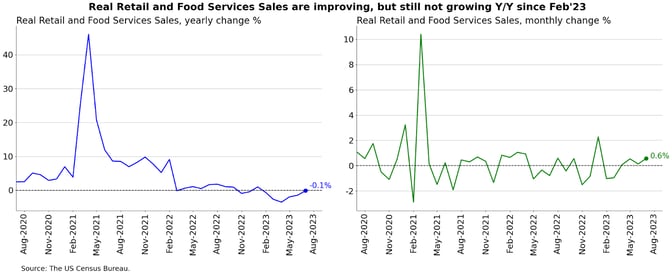

Real retail sales rose 0.5% MoM in July, and August data should show further gains once it is available - Figure 5. According to the National Retail Federation, "consumers are expected to spend record amounts on both back-to-school and back-to-college shopping this year," boosting sales for another month.

August typically sees a MoM inch up in sales due to back-to-school and end-of-summer sales. It is also the start of the peak season for the freight industry.

Figure 5

The monthly increases in retail sales since March have so far not been enough to push the year-on-year growth rate above zero. Freight volumes are also still at a low level compared to last year (Loadsmart volumes are down 18% YoY and Sonar OTVI volumes are down 10% YoY).

A strong back-to-school season can be a sign of a better holiday season to come. If it is confirmed to be stronger than last year, it may indicate that we have a better holiday season ahead.