Share this

A recent roundtable discussion featuring George Swartz, Michael Munday, Melissa Collins of Loadsmart, and Jim Lane of Redbank Advisors highlighted some perspectives on the current logistics market and what each sees as positive indicators for 2024 and beyond. Each brought several interesting insights (along with some optimism) to the panel.

Here are some webinar highlights

The discussion started with a positive reminder. Although the logistics market has had its challenges of late, this isn’t the first time the economy or the industry has been through tough times. The freight market is constantly changing, and it has been more challenging based on several measures many times in the past. Cyclical by nature, these things always turn around and get better after downturns. And while recovery is sometimes slow, it does happen. Overall, the panel agreed there’s solid data-backed evidence that the current market conditions are easing and things are already trending in a positive direction.

It was also observed that, although the industry took its share of hits from COVID, some parts did well—or even boomed in certain cases. The number of people shopping online created a spike in demand in many parts of the logistics industry, mainly after governments injected cash into the economy. Yet, while demand for warehousing and space on ocean container ships drove up rates, much of the spike was due to artificial growth.

We’re in a recovery

So today, as the market continues to normalize, the recovery is happening, albeit in some uneven ways. Earnings growth has resumed for many types of shippers, driving up demand for freight services. But in some sectors, like industrial, recovery has been slower.

Based on reported company earnings growth in Q3 and Q4 and optimistic projections for Q1 and Q2 of 2024, the panel feels the economy is getting healthier. There’s hope that rising demand and economic activity will continue into 2025 based on what’s happening now. Signs of disinflation also point to a positive future for the logistics industry.

The panel cited recent Loadsmart market data supporting the idea that such freight business cycles typically last about three years, with the most recent ‘trough’ happening in the Spring of 2023. Since that time, things have been on a positive trend. The data suggests that if there are no significant disruptions to the industry or economy in the short term, the current cycle should remain on that upward trend until at least 2025. The expectation, however, is that the cycle won’t be as steep as it was during the last COVID-driven upcycle. It will be a more gradual increase, led by limited transportation capacity and carriers leaving the market, instead of the skyrocketing demand that occurred last time.

Other market indicators

Tender Rejections

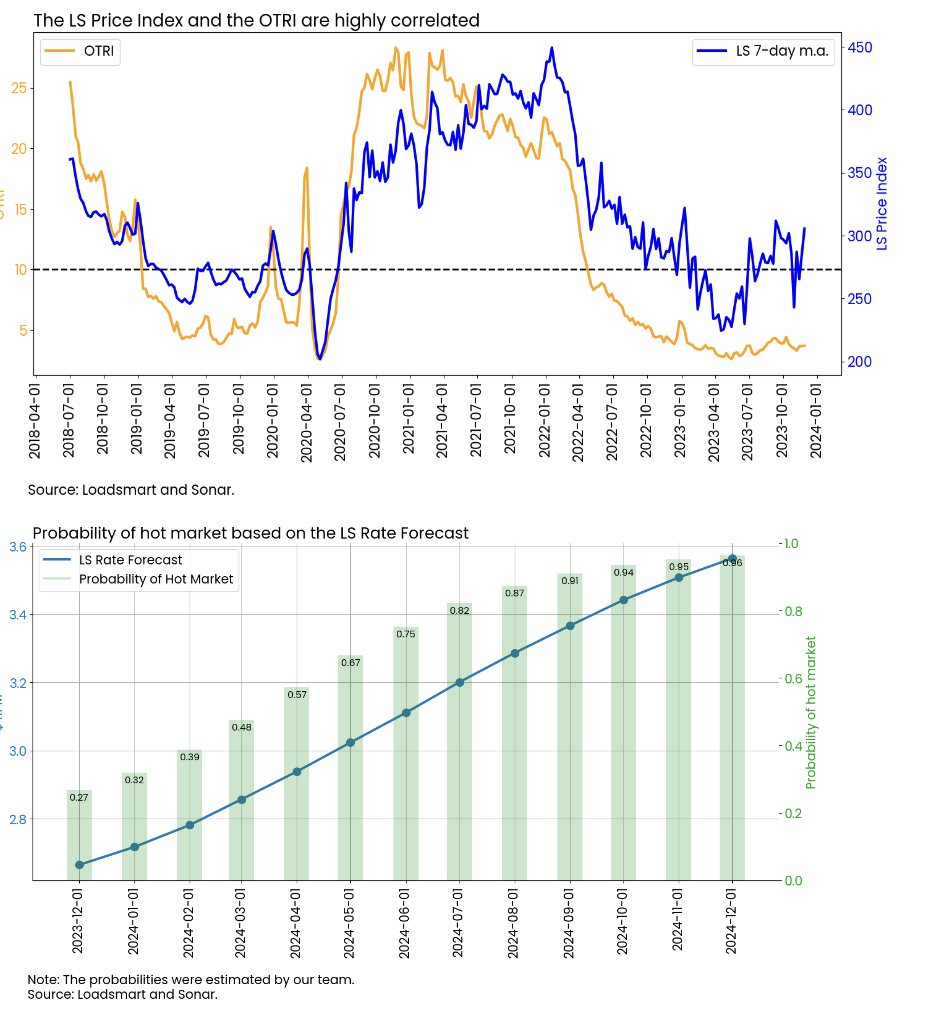

Other transportation market indicators from recent reports, although not exactly what shippers want to hear, include a slight increase in tender rejections and volume, supporting the claim that the market has already reached a bottom and reversing its trajectory. Loadsmart’s modeling shows a strong probability that by July 2024, tender rejections should exceed 10%, a benchmark considered an indicator of a ‘hot market.’ This, the panel agreed, is more proof the market is heading in a positive direction.

Carrier Rates

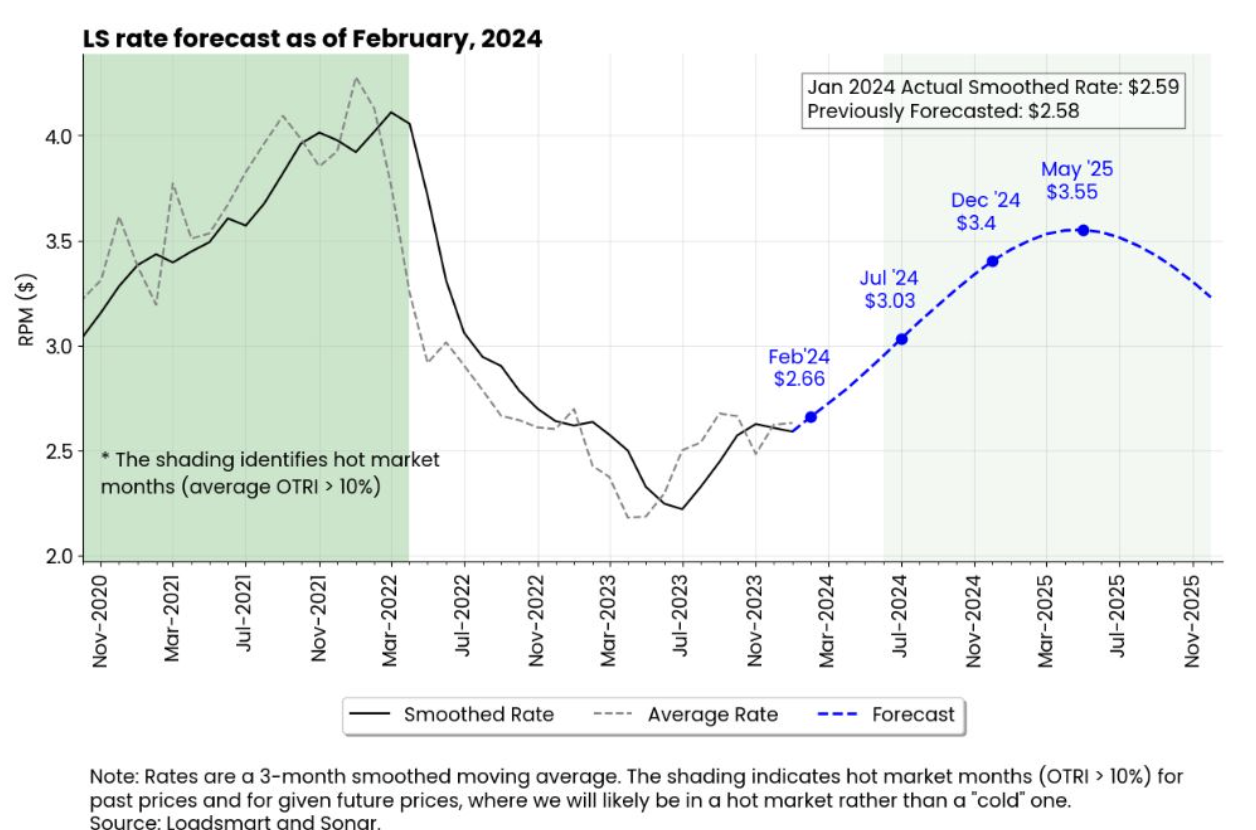

The panel offered some projections regarding carrier rates. By the end of the year, Loadsmart sees the national all-in price per mile at about $2.60 at the end of 2023. Rates will continue to rise to $3.20 in July, then end 2024 at about $3.56. In the panel’s opinion, although it feels like a significant increase, this is a mild recovery from the carriers’ perspectives. Even at over $3.50 per mile, the market won’t be anywhere near as expensive as it was at the top of the last cycle.

Freight Volume at Ports

Another important market indicator is that freight volumes are building back up. Import volumes are growing at key U.S. ports. Looking at the Port of Los Angeles specifically, starting with the end of Q3, the port had about a 6% increase in the number of containers processed over the same time last year. The Israel-Gaza war is now impacting supply chains, and if the situation continues, we expect to see an increase in truck and intermodal demand out-bound from the West Coast (read further on our January Loadsmart Look Ahead blog post). Furthermore, the American Trucking Association, which has its own forecast, expects truck tonnage to grow from about 11.3 billion tons in 2024 to 14.2 billion in 2034.

Intermodal and Air

Due to those growing imports, a significant increase is also expected for rail and intermodal volumes, with the jump from around 22 billion tons in 2023 to 35 billion in 2034. And air cargo, which is sitting at about 18 billion tons this year, is expected to rise to 23.7 tons in 2034.

The outlook is... positive

The tone of the discussion was positive, and there are many reasons to feel a recovery for the logistics market is underway. And, Loadsmart’s market projections show the improvements are still in the early stages.

A stronger logistics market can result in higher rates for shippers, so the panel’s observations and predictions come with a warning. Now is the time for companies to look closely at their rates and take steps to insulate themselves against any cost increases going forward. The market is shifting, and shippers should be prepared to keep their supply chain costs and service optimized for however the market looks in 2024 and beyond. Take advantage of Loadsmart’s Free Transportation Savings Assessment to uncover hidden savings and optimize your logistics.