Share this

by jpallmerine

As usual, in this Monthly Market Update, we will provide a brief update & analysis of the full truckload market and present some compelling trucking-related economic analysis to provide a macroeconomic view on the state of the market.

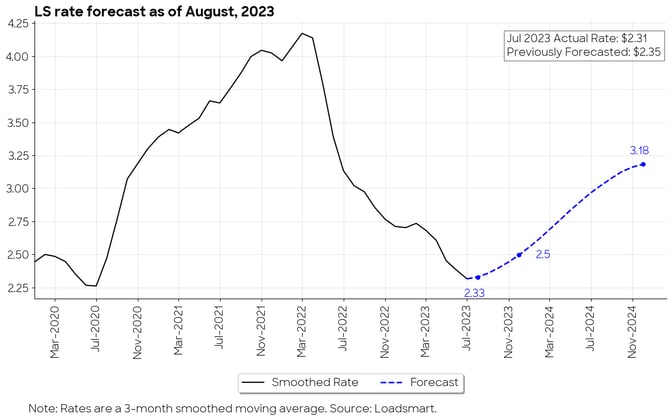

As of August 1, 2023, our model predicts that the average spot price should have bottomed out in July, rising from $2.31 to $2.33 in August.

By the end of 2023, our forecast calls for prices to rise to $2.5 (an 8.2% increase from July's low) and continue on an upward trajectory through 2024.

Figure 1

August's Full Truckload Market Overview:

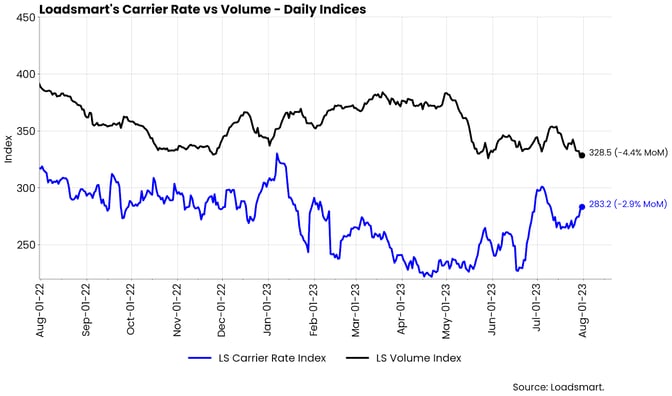

Rates: Our price index decreased by 2.9% MoM in July. The price spike associated with the 4th of July holiday brought the index back to January 2023 levels. However, as we predicted in the previous report, the index later pulled back ~10% from the July 4th high and remained stable throughout the month till the 25th, when a new upward trend started.- We attribute the most recent upturn in prices to be mostly driven by the rise in fuel surcharges in the last week of July (see more in the Freight & Economics Section) as well as some minor tightening from EOM.

Volumes: Our volume Index decreased by 4.4% MoM in July. Sonar's OTVI rose 5% over the same period, but Loadsmart has yet to see the reported increase in freight demand, either in quotes or allocated volumes.

- The only region where volumes recovered significantly was the Northeast, where volumes have been growing since July after a stagnant 2Q.

Figure 2

Freight & Economics

Soaring Fuel Prices

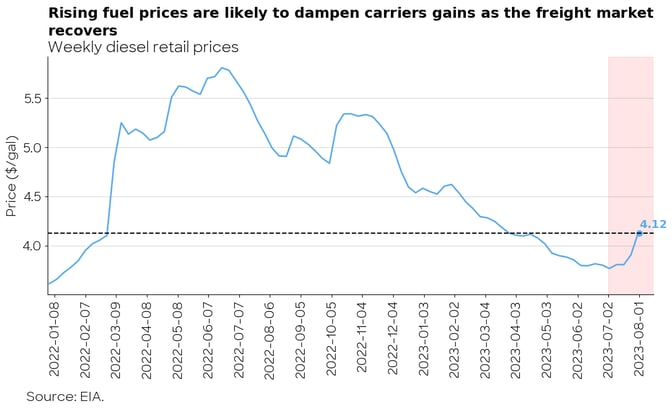

Diesel prices rose 9.5% in July - back to April levels, as shown in the figure below.

Figure 3

According to our estimates, part of our rate price upturn in the past week (July 28- Aug 5), shown in Figure 1, was due to the increase in fuel surcharges. Our all-in carrier RPM rose 4% WoW, but our line-haul rates show an increase of 2% only.

We expect fuel pump prices to continue to hike in the next months, which would further damage spot market profitability for smaller carriers. EIA's latest forecast (from July 6) indicated that diesel prices would average $3.76 in July and $3.58 in August. But we now know that July's average was 10 cents higher than their prediction, and August should be higher as well.

Here are the main reasons why we believe fuel prices should rise further in August:

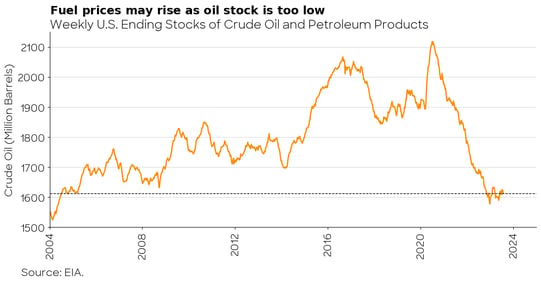

- Supply Cuts: As mentioned in March’s Monthly Update, Opec announced a production cut that began in May and will run until the end of 2023. Additionally, the US crude oil production is also declining. National inventories are at their lowest levels in more than a decade - as shown in Figure 4.

Figure 4

- Expected Demand Boost: Fuel consumption should rise along with household spending in the coming months as a recession-free soft landing becomes more likely.

Freight Sector Revenues

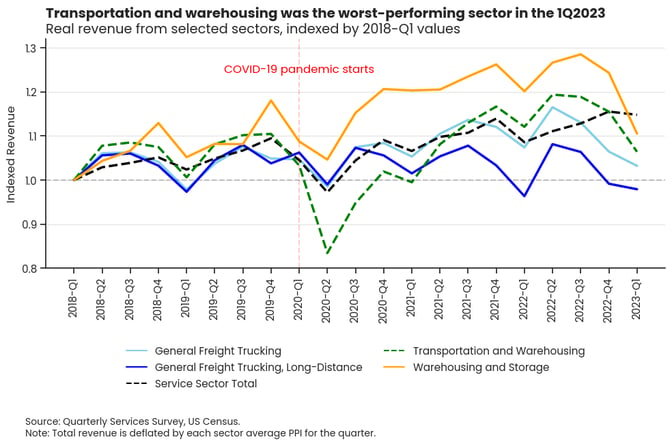

According to the US Quarterly Services Survey, transportation and warehousing had the largest revenue decline among all services sectors in 1Q2023, with its real revenue falling 7.8% QoQ.

Figure 5

Warehousing appears to be the main driver of this large decline, as its real revenue alone fell 11%, while the general and long-haul trucking categories fell 1.2% and 3%, respectively.

The real revenue of the whole services sector decreased by 0.6% QoQ (Figure 5). The first quarter of the year is typically characterized by a seasonal decline in revenue. However, for the trucking categories, this is the third consecutive decline in revenue and may be related to the decline in freight rates that also began in Q2 2022.

We do not expect revenue growth in the next report due to the continued decline in freight rates in Q2 2023, but we’re optimistic that this could begin to switch positive by the end of 2023.

Please reach out to Stella Carneiro (stella.carneiro@loadsmart.com) with any questions, suggestions, thoughts, etc. Thank you! We hope you enjoy! #movemorewithless